Archer. The Flying Taxi Company

[8 minute read] Is this flying taxi company defying all odds to launch a flying taxi by 2024, or is it too ambitious for its own good?

Archer is an interesting company to analyze. The company wants to build flying taxis… flying taxis of all things! It’s an ambition that feels a bit too futuristic to be realistic, especially for a burgeoning public company with zero revenue.

Archer went public through a SPAC during the pandemic bull market and like many SPACs of this era, the company was nowhere close to being ready for the public spotlight but was hurried into public markets by Wall Street’s misguided eagerness (and perhaps greedyness) to sell stocks. However, unlike most of its SPAC peers, Archer’s stock didn’t completely crash. After two years as a public company, the stock seems to have revived, jumping from under $2 to almost $7 this year as the company appears to be on-track to launch its first aircraft, Midnight, by 2024.

Does this flying taxi company actually have wings, or is it too ambitious for it’s own good?

Let’s find out.

Archer’s goal is straightforward. The company wants to “find the most efficient path to commercializing world-class eVTOL (electric Vertical Take-off and Landing) aircraft as safely as possible”.

Why eVTOL Aircraft? Answer: Flying Taxis

VTOL aircraft combine the super-short takeoff and landing capabilities of helicopters with the faster and heavier transport capabilities of fixed-wing aircraft. Electric engines make them more environmentally-friendly than gas turbine or jet engines. This makes eVTOL aircraft a perfect short-range rapid transportation option in traffic-dense urban centers like cities. In other words, eVTOLs make for great flying taxis.

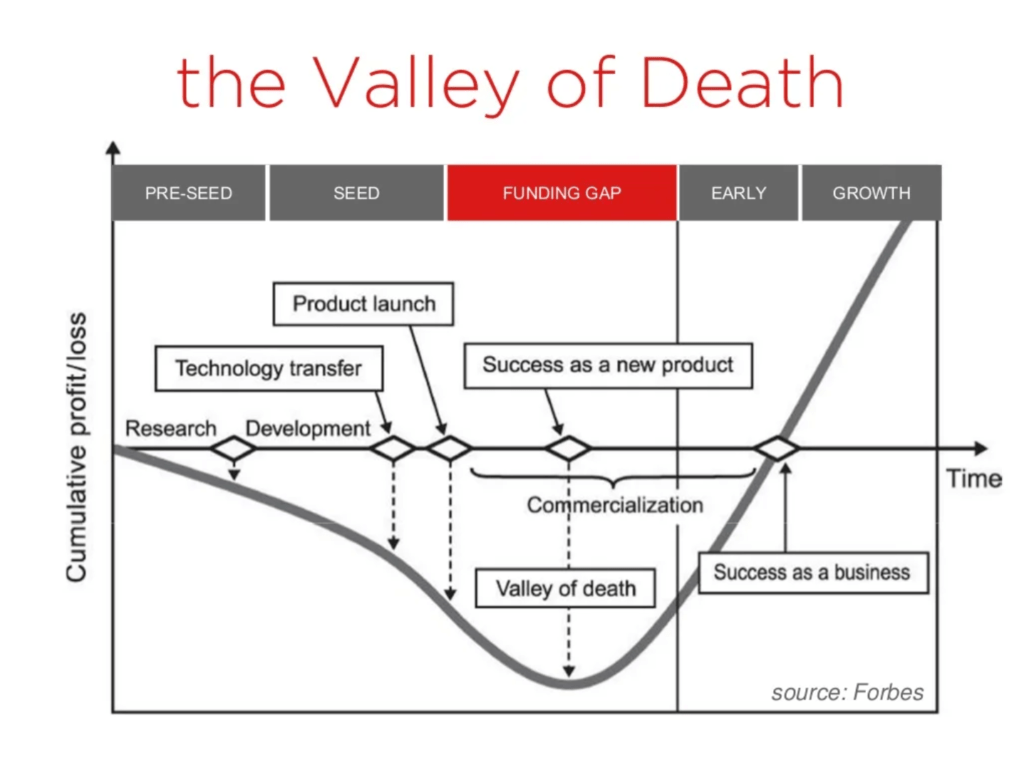

Valley of Death

Commercializing a new aircraft is hard. Commercializing a new aircraft that’s as unconventional as an eVTOL aircraft is extraordinarily hard. The technology is hard, the manufacturing is harder, and working with regulators is even harder.

A term to describe common private sector failures in heavily-regulated industries is the “Valley of Death”. This valley occurs between the successful demonstration of a prototype, obtaining regulatory approval, and experiencing commercial success. Many early-stage companies often become insolvent while traversing the valley.

Can Archer Survive?

The short answer is a resounding yes.

Archer appears to be more than adequately set up to fly over the Valley of Death. The company has established a series of partnerships with industry heavyweights and the US military to build capital-raising momentum. This momentum has helped it raise $1.1 billion to date, with $675 million on hand.

A Little Bit on Archer’s History

Archer was founded in 2018 by two software entrepreneurs, Brett Adcock and Adam Goldstein. Prior to Archer, Brett and Adam co-founded an employment marketplace website called Vettery that was sold to Adecco Group for $110 million.

It’s surprising that with just the experience of building a website company, Adcock and Goldstein were able to leverage their business acumen to get an aircraft startup to be as successful as Archer is today.

On further research, I learned that the two entrepreneurs appeared at the right place and at the right time to skillfully capitalize on two important opportunities.

First, Airbus was already working on eVTOL technology in the US through a subsidiary called Vahana. For whatever reason, Airbus decided to move the entire operation to France, leaving many of its staff stranded in the US. Second, US company Kitty Hawk was also working on eVTOL technology but most of its staff was disgruntled after a Boeing acquisition. Adcock and Goldstein swooped in to hire both teams to form Archer’s starting team.

Successfully getting both Airbus’s and Boeing’s teams into Archer is not just a foot-in-the-door for the aviation industry, it was an honorary reception.

Where Is Its Technology At?

Archer’s first aircraft is a 2-seater eVTOL technology demonstrator called “Maker”. Maker completed its first flight on December 16th, 2021.

Its first planned production aircraft, “Midnight”, is still under development. A completed prototype was revealed in May and the Federal Aviation Administration (FAA) recently issued a special airworthiness certificate for the aircraft which allows it to be flown for testing.

Archer hopes to have Midnight commercially certified in 2024.

The aircraft has a range of 50 miles (80 km) and a cruise speed of 150 mph (241 km/h).

Partnerships

As alluded to above, starting a new aircraft company on one’s own is extraordinarily hard. As such, a key pillar of Archer’s business strategy is to establish partnerships with industry giants that will make its eVTOL production line possible. Archer has done this in spades:

United Airlines: The company is a major investor in Archer and has even placed a $1 billion order for Midnight aircraft.

US Air Force / Department of Defense: Archer has been working with the DoD since 2021 through the Air Force’s AFWERX program. This August, Archer secured a $142 million contract with the US Air Force that involves delivery of 6 Midnight aircraft.

Boeing and Wisk: Boeing, through its subsidiary Wisk, had originally sued Archer over stolen trade secrets but the company has completely reversed its stance, settling the lawsuit with Archer and investing in Archer’s recent $250 million fundraising round alongside Stellantis and United Airlines.

Stellantis: The company is a major investor in Archer that will also play a pivotal role in mass-producing the Midnight. The company will contribute “advanced manufacturing technology and expertise, experienced personnel and capital” to make the Midnight production line possible.

Abu Dhabi: Archer signed a memorandum of understanding (non-binding agreement) with Abu Dhabi to provide an air taxi service for the city in exchange for incentives to establish its first international headquarters and manufacturing facility in the city.

Risks

Archer’s business has three main risks: risk of execution, risk of regulation, and risk of valuation.

Companies at Archer’s stage typically have a fourth risk, that of capital, but Archer has $675 million in cash with options to raise more so we don’t think capital is a risk for now.

Risk of Execution

It’s one thing to raise money and establish partnerships, it’s another to design, test, and mass produce a safe eVTOL aircraft. VTOL aircraft is more complex than normal helicopters/fixed-wing aircraft and is thus more dangerous to operate. It’s no coincidence that the US military’s only operational VTOL aircraft, the V-22 Osprey, has a reputation for being unsafe.

Now, combine the challenges of a VTOL aircraft with the novel use of electric aircraft motors and one can see that Archer has very high-flying ambitions.

A widely available eVTOL air taxi service in cities worldwide might be an enticing dream but the path to get there is far from easy. What happens to the company if a mishap occurs? Could a hidden design flaw cause a series of mishaps?

Consider the world’s first commercial jet liner, the de Havilland Comet: within a year of the airline’s entry into service, 3 Comets were lost in highly publicized accidents after suffering catastrophic mishaps mid-flight. The Comet was pulled from commercial use and redesigned, but sales never fully recovered. Could this happen to Archer?

Risk of Regulation

Heavy-handed regulation freezing progress is a big concern for any project as unconventional and uncertain as flying taxis. Archer might have a lot of money to survive for a long time in the Valley of Death but what if the flying taxi Valley of Death is impossibly large?

Thankfully, it appears Archer is working closely with the FAA. They’ve so far experienced fledgling success with the regulator: the FAA gave the Midnight prototype a special airworthiness certificate earlier this year and have also approved some of the commercial certification plans for the aircraft.

However, Archer is just at the base camp of the massive regulatory mountain they need to summit. Even if the FAA certifies the Archer in a timely manner, state and local governments have to approve the use of eVTOLs as flying taxis as well.

Risk of Valuation

Archer’s stock could still be significantly overvalued now even if its business plan is eventually successful. If so, investing in the company now will result in a lackluster or even disastrous investment for a long time before its stock price recovers.

We’ll discuss more about valuation below.

Valuation

Archer is currently valued at $1.23 billion. Because the company is still at the prototype stage, and the size of the currently non-existent flying taxi industry is unknown, it’s incredibly difficult to valuate the company.

One could compare Archer to its industry peers but how many public eVTOL companies are out there? The answer is basically none besides Archer (☝️actually, there’s Joby Aviation). As such, to find adequate peers for Archer, we’ll have to settle for similar-stage companies in an adjacent industry and Space is a good one.

Two public burgeoning Space companies fit Archer’s profile: Rocket Lab and Virgin Galactic Holdings.

The low cashflow nature of early-stage companies makes it hard to find an appropriate financial yardstick to measure the companies by. I’ve picked the Price-to-Book ratio (PB ratio) to compare Archer and its peers. The PB ratio measures a company’s market valuation against the net value of its assets.

Using the PB ratio yardstick, we see that Archer is on the expensive end: the company has a PB ratio of 4.7, Joby is at 3.6, Rocket Lab is at 3.3, and Virgin Galactic is at 1.2.

Does Archer deserve a higher valuation from its peers due to its extensive partnerships and on-track business plan? For pre-production companies like Archer, no one really knows.

Fin

If you think flying taxis will be a massive industry, then Archer is fantastically set up to capitalize on this yet-to-exist business. The company is not only heavily-capitalized and well-partnered, it’s basically the culmination of both Airbus’s and Boeing’s efforts in the past decade to make eVTOLs possible.

However, no matter how well the company is set up, it’s still in the prototype stage for a product that’s meant to serve a non-existent industry. That is a LOT of risk.