Thoughts - Free Cash Flow!

In times of uncertainty, investors look for safety. In practice, this means the market turns to Free Cash Flow. This article discusses Free Cash Flow and its relevance to current market conditions.

In early May of this year, a letter sent by Uber CEO Dara Khosrowshahi to Uber employees was leaked to the financial press. The letter opened with this momentous statement:

“After earnings, I spent several days meeting investors in New York and Boston. It’s clear that the market is experiencing a seismic shift and we need to react accordingly.”

From the get-go, you could tell this was an important letter. In it, Dara gave a brief overview of the state of the broad market and then discussed Uber in detail, including where the company is headed, its current standing among institutional investors, and how it compared to arch-rival Lyft. Dara had this to say about the broad market:

“In times of uncertainty, investors look for safety. We have made a ton of progress in terms of profitability, setting a target for $5 billion in Adjusted EBITDA in 2024, but the goalposts have changed. Now it’s about free cash flow. We can (and should) get there fast. There will be companies that put their heads in the sand and are slow to pivot. The tough truth is that many of them will not survive… Rest assured, we are not going to put our heads in the sand. We will meet the moment.”

The TLDR, if you may, is that in this new market environment, Free Cash Flow has supplanted Growth as the most important yardstick to measure a company by. Before diving deeper into how Free Cash Flow is relevant to current market conditions, let’s go over what it is.

What is Free Cash Flow?

A “good” company, at a high level, is simply one that makes money. In other words, a good company earns more money than it pays out (unless the money is being paid out to shareholders).

Say No to Profit

One way to measure whether a company makes money is through its Profit, which is found on the Income Statement by subtracting Expenses from Revenue (a very rough approximation, but you get the point). On first impression, this sounds like it’ll do the trick, but the accounting definitions of Revenue and Expenses make them poor representations of how much money a company is actually making.

There are two primary reasons for this.

First, the accounting standard used by the US (called GAAP, or Generally Accepted Accounting Principles) allows companies to turn large capital expenses into smaller non-cash expenses such as depreciation and amortization on the Income Statement.

For example, if a business buys an $18,000 factory machine that it expects to last for 36 months, then the $18,000 upfront cost can be turned into a $500/month ($18,000/36=$500) depreciation expense on the Income Statement. In reality, the company lost $18,000 in one go, but GAAP allows this huge purchase to be split into small chunks of expenses over time which makes the company’s current Profit look better than it actually is.

The second problem with Profit is the fact that Revenue can be recorded well before the entire payment from a sale is received. For example, if a sale is made on credit and the collection period is over a year, the full amount of the sale can be recorded as revenue at the time the sale was agreed upon, even if the company hasn’t received the full payment.

In general, Profit on the Income Statement has a lot of noise which can obscure a company’s actual performance. This also makes it a lot easier for a company to manipulate its Income Statement to make things look better than they actually are. Cash Flows, on the other hand, present a clearer picture and is much harder to manipulate without being explicitly malicious.

Free Cash Flow

To understand Free Cash Flow, we need to first understand the broader concept of cash flows. Cash flows are exactly what their name implies: the movement of cold, hard cash in and out of a company. Companies report their cash flows through Cash Flow Statements.

One perk with cash flow reporting is that it’s really hard to “cook the books” with them. In other words, there are few fancy accounting rules that one can use to hide unfavorable cash movements to window dress Cash Flow Statements.

Going back to the example of the $18,000 factory machine purchase, although it can be turned into a $500/month depreciation expense on the Income Statement, it’s a clearcut outflow of $18,000 on the Cash Flow Statement. There’s no way to hide it (unless one commits accounting fraud).

Cash flows are generally split into three categories:

Cash Flow From Operating Activities (CFO)

Cash Flow From Investing (CFI)

Cash Flow From Financing Activities (CFA)

CFO is the net cash received or lost from a company’s operating activities. It’s typically calculated by starting with cash received from sales and subtracting cash paid to suppliers and employees, cash paid to meet debt interest payments, and cash paid for government taxes. Among the three types of cash flow, CFO is the most closely tied to a company’s performance.

CFI is the net cash received or lost from a company’s investing activities. Examples of investing activities include acquiring other businesses, buying a new building, or investing in Bitcoin (* cough * Tesla * cough *). Since healthy companies are usually investing rather than divesting, CFI flows are typically negative.

Finally, CFA is the net cash received or lost from a company’s financial activities. These include issuing and selling new shares (cash received), taking out a loan (cash received), or issuing dividend payments to shareholders (cash paid out).

With the three basic types of cash flows covered, we can explain Free Cash Flow, the namesake of this newsletter issue.

Free Cash Flow is generally found by subtracting cash paid for long-term assets (a portion of CFI known as Capital Expenses) from CFO. This gives us cash that a company gets to keep after all the company’s maintenance and growth obligations are covered.

A more personally relatable way to think of Free Cash Flow is the amount of your salary that you can spend on whatever you feel like after you’ve paid for essential living expenses like food and housing.

Value investors love Free Cash Flow. Not only is it hard to manipulate, it also gives a clear picture of a company’s survivability and profitability.

Caveat

Although Free Cash Flow is a powerful tool to understand a company’s financial standing, GAAP doesn’t officially define what it is. As such, companies can differ in how they calculate Free Cash Flow.

For example, although it’s generally understood that Free Cash Flow is found by subtracting Capital Expenses from CFO, ExxonMobile adds cash received from investment returns and the selling of company assets to their version of Free Cash Flow. General Electric does something similar.

So What? (Lessons From 2022)

As inflation heated up in 2021 and the economy worsened with supply chains constrained by lockdowns in China and the war in Eastern Europe, the market quickly pivoted from prioritizing Growth to prioritizing Free Cash Flow.

Harking back to Uber CEO Dara Khosrowshahi’s leaked company letter, Dara wrote that “[i]n times of uncertainty, investors look for safety”, and Free Cash Flow is the market’s favorite yardstick to measure the relative safety and quality of companies.

The market’s pivot to Free Cash Flow was first evident in the early valuation drops of high growth, low Free Cash Flow mid-cap companies like Palantir and Shopify in Q4 2021. During this time, the S&P 500 was unscathed and even continued climbing. However, the contagion spread fast and by the turn of the year, large-cap companies were also subject to this same new valuation rubric. The market wanted Free Cash Flow and it wanted it now.

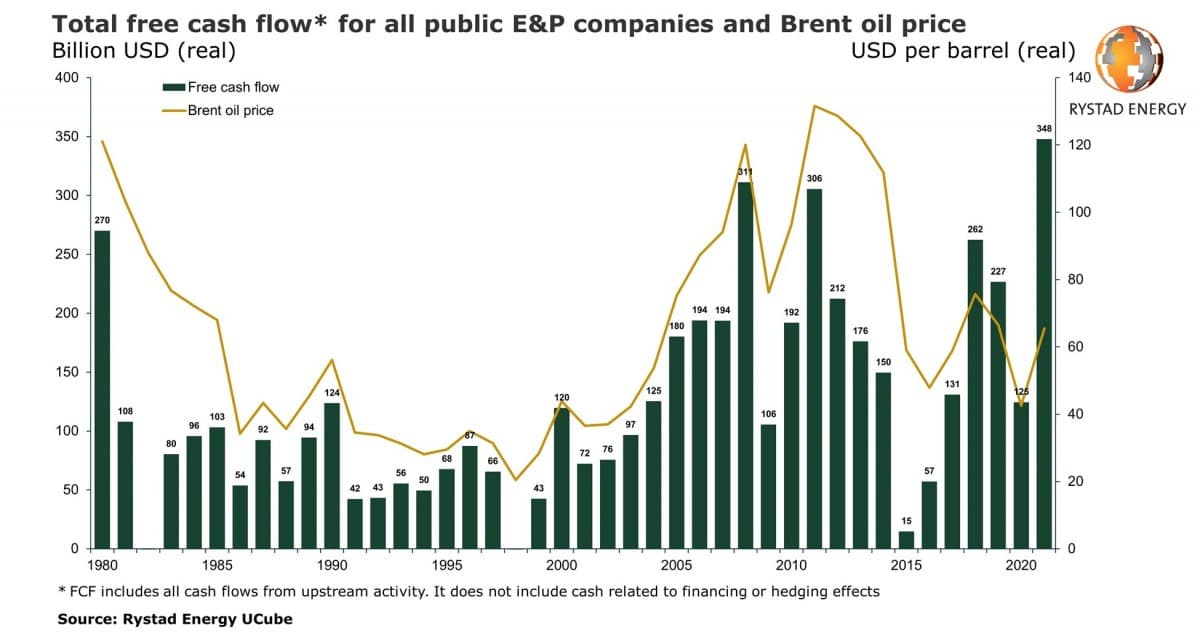

Oil Price and Free Cash Flows

Not surprisingly, as oil prices rose, the Free Cash Flow generated by energy companies surged as well. While the rest of the market tanked in Q1 2022, energy companies were bought up by speculators and investors looking for the safety of their cash flows.

Stock-Based Compensation

Stock-based compensation (SBC) is where companies pay employees with shares (typically newly issued) rather than cash. The main benefit of SBC is the fact that it doesn’t affect a company’s cash position at all and thus doesn’t show up in Cash Flow Statements. This can significantly improve the appearance of said statements.

Over the past year, several companies have started to draw scrutiny for their excessive use of SBC. This over-reliance on issuing new shares to pay their workforce felt like an abuse of the cashless perk of SBC to improve the company’s financials.

Robinhood and Coinbase are two such companies. The two gave out $1.57 billion and $821 million in SBC in the last year, respectively. Keep in mind, these are billions of dollars leaving the company that don’t show up in their Cash Flow Statements. The SBC bonanza at both companies continued in 2022, with Robinhood giving out $220 million in SBC in Q1 2022 and Coinbase giving out $352 million in SBC in the same period.

By heavily relying on SBC to pay employees, both companies are essentially shielding their Cash Flow Statements from billions of dollars of payroll expenses while also taking money from existing shareholders through excessive share dilution.

As such, when considering a company’s Free Cash Flow, one needs to be careful of SBC. A good way to remove SBC risks from financial analyses is to normalize business metrics by share count (e.g. use Free Cash Flow per Share instead of just Free Cash Flow).