Market Forecast - A Big Week!

This is a big week. GOOG, MSFT, META, AMZN, and AAPL are all reporting earnings this week. Another large interest rate hike. June's inflation data. Q2 GDP. Let's discuss and forecast!

FinanceTLDR is donating to a positive cause every month. For this month, we’re donating to the SF-Marin Food Bank. We hope that this is a more direct and effective way of addressing the most immediate needs of the homeless.

Don’t feel pressured to join us, we simply ask that we all do a little extra good this month, whether for a cause you believe in, a friend, a loved one, or even for yourself.

This is a big week! Alphabet, Microsoft, Meta, Amazon, and Apple will report Q2 earnings. On Wednesday, the Federal Reserve will announce the size of their next interest rate hike. On Thursday, we’ll get an advanced estimate of Q2 GDP. On Friday, we’ll get June’s PCE inflation number.

For a full discussion of the major events happening this week and how they’ll affect the market, check out the Market Forecast section below.

At a Glance

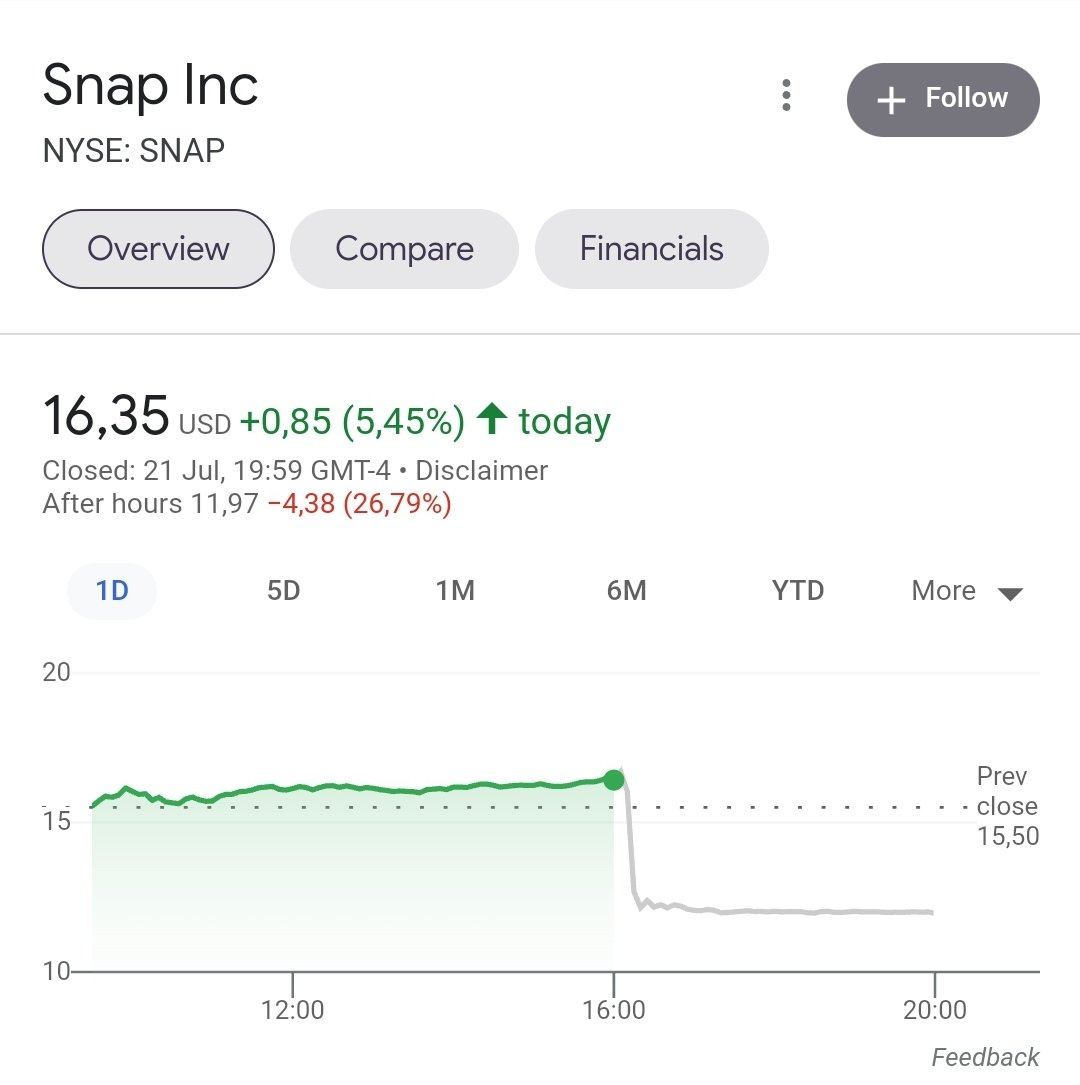

SNAP Just Can’t Catch a Break!

SNAP just can’t catch a break! After dropping over 35% in May when Evan Spiegel warned that the company will miss its revenue and earnings targets for Q2, the company's actual Q2 results (reported last week) still underperformed the deflated market expectations. The stock fell over 25% after the earnings call.

This once high-flying pandemic stock is struggling with a contracting ad market from uncertain economic conditions and the meteoric rise of TikTok. TikTok pulled in $4.6 billion in revenue last year and is expected to almost triple revenue this year to $12 billion. Tripling revenue in one year for a company at the scale of TikTok is unheard of and it’s putting every ad publishing company on edge.

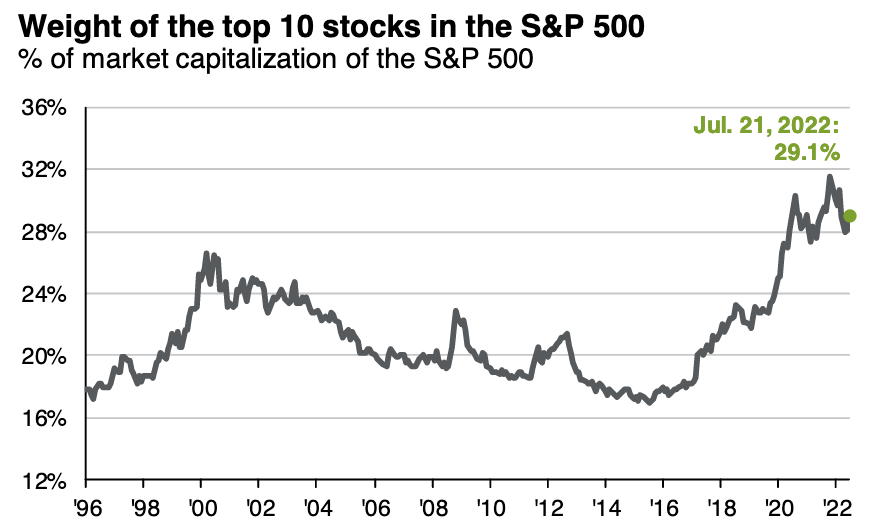

A Top Heavy Stock Market

The Short: The overwhelming success of big tech companies with their high-scale, asset-light, and international business models have resulted in their stocks crowding the top of the S&P 500 index. Just five big tech companies, Apple, Microsoft, Amazon, Alphabet, and Meta collectively represent a massive 21% of the 500-company index!

The Long: Although the rapid growth of these companies have made S&P 500 investors a lot of money, their disproportionate size in the index creates significant risk for the market as problems in any of them could trigger a significant market correction. Examples of risk factors include a geopolitical conflict in Asia disrupting Apple’s supply chain, anti-trust regulation against Amazon, Alphabet, or Meta, or the sudden emergence of a highly successful but private company competing away big tech’s lucrative ad margins (* cough * TikTok * cough *).

Apple, Microsoft, Amazon, Alphabet, and Meta are all reporting Q2 earnings this week. Their results will set the tone for the market.

China Is Divesting From US Treasuries

The Short: China, the second largest holder of US treasuries, has been steadily selling off treasuries. The size of their treasury holdings fell in May to $980.9 billion, the lowest it’s been since May 2010.

The Long: This is a worrisome sign for the geopolitical situation in Southeast Asia.

In 2018, Russia suddenly dumped 84% of its $100 billion portfolio of US treasuries. Given the ongoing conflict in Eastern Europe, we can say from hindsight that this treasury sell-off was likely part of an overall decoupling process from the Western economic system in anticipation of said conflict.

As for Southeast Asia, the worst case interpretation of China’s ongoing divestment from US treasuries is the anticipation of conflict with Taiwan in the not-so-distant future. Over the past year, US-China tensions have risen dramatically over Taiwan. Biden vowed in May to defend the island nation if China attacked while Speaker of the House Nancy Pelosi plans to visit Taiwan in August. US policy towards Taiwan appears to be shifting from a more subtle and supportive approach to one that’s more hands-on and assertive.

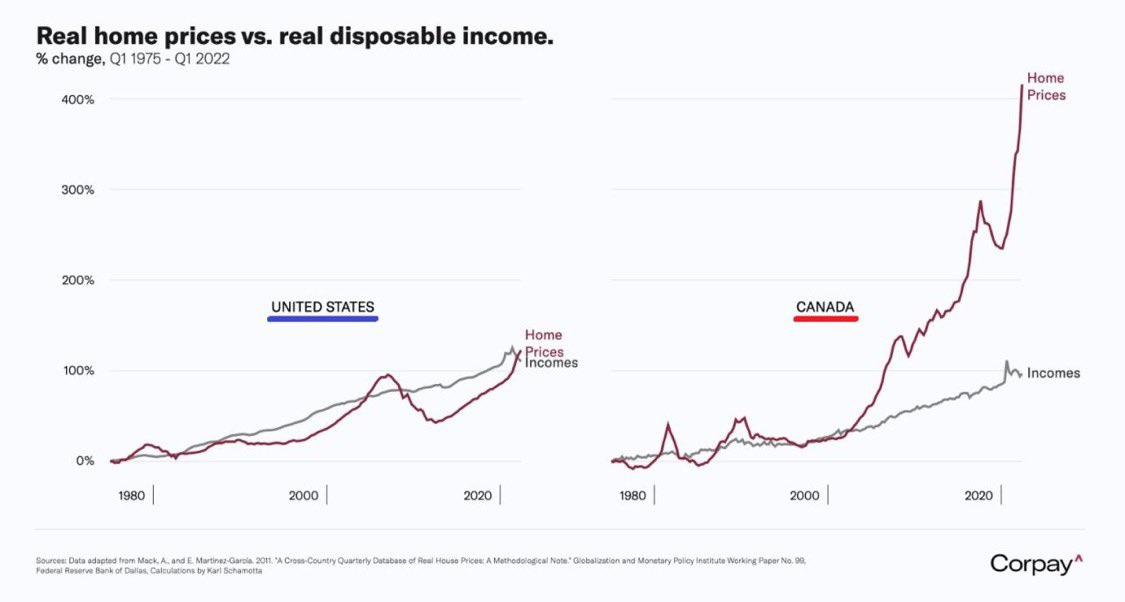

Not For the Young

The Short: Canada’s soaring real estate market has completely outpaced wage growth in the country. This has effectively funneled significant wealth to international investors and the country’s older generations. Many young Canadians, who are just now entering the work force, will find it incredibly hard to build wealth. Much of their income will be siphoned off for transportation and rent (which loosely tracks real estate prices) and little is spared for acquiring assets.

The Long: The strongest driver of the Canadian real estate market is foreign investors (especially from China). Chinese investors seek to diversify wealth from China but want to avoid the US given rising US-China tensions. Canada is the next best alternative. Unfortunately, the Canadian government is ill-equipped to handle such a large influx of wealth and has followed the path of least resistance by allowing the wealth to pour in, thus benefiting the old and hampering the youth.

Market Forecast

The market is currently split between two narratives. Inflation appears to be cooling, which bodes well for the market, but people are worried that Q2 earnings will disappoint and push the market lower. After this eventful week, we will have a lot more clarity on which narrative is winning. The major market events happening this week are:

Big Tech Earnings

Alphabet (Tuesday), Microsoft (Tuesday), Meta (Wednesday), Amazon (Thursday), and Apple (Thursday) are reporting Q2 earnings this week. Collectively, they represent more than a fifth of the S&P 500 and any weakness from this group will push the market lower.

So far, the prospects for positive results are poor given the widespread hiring freezes and publicized notes from CEOs on the need for tighter cost controls. In addition, the market is using SNAP as a bellwether for big tech and the company’s disappointing Q2 earnings call is being interpreted as a sign of a bad quarter for big tech.

Next Interest Rate Hike

The Fed will announce the size of its next interest rate hike on Wednesday. The market is predicting a 75-basis-point hike (80% chance) but there’s a good chance it’ll be a 100-basis-point hike (20% chance) instead.

Inflation is hard to fight, and it might be too optimistic for the market to rally after the first signs of cooling inflation in June. An early market rally could easily trigger the next bout of inflation. As such, we think the Fed won’t hesitate from overaggressive rate hikes to really clamp down on inflation. If so, they will raise by 100 basis points and the market will react poorly to it.

PCE Inflation Data

June’s PCE inflation number is set to be released on Friday. Although the public is more familiar with CPI as a measure of inflation, the Fed prefers PCE. It’s a broader and timelier measure of consumer behavior than CPI (e.g. significantly less weight on shelter).

With crashing energy and commodity prices in the past two months, many are expecting PCE inflation to fall meaningfully in June. If so, it’ll by well received by the market as a confirmation of cooling inflation.

Q2 GDP

We will get an advanced estimate of Q2 GDP on Thursday. This number is not as helpful to the market as the prior three pieces of information. Sure, if Q2 GDP is negative, we’ll have two consecutive quarters of negative GDP. Some interpret this as a sign that we’re in a recession. At FinanceTLDR, we think that the US economy is nowhere close to a practical recession.

The Forecast

Although we believe there’s more short-term downside to come, too many major events are happening this week to make a meaningful market forecast. Big tech earnings are likely to disappoint but we’re also not a fan of trading earnings. Another major unknown is Jerome Powell’s press conference on Wednesday after the Fed’s interest rate announcement. The market tends to cling to his every word and he could make exceedingly bearish or bullish comments.

As such, if you’re trading, we still think it’s best to keep risk off the table. If you’re dollar-cost averaging into investments, you can ignore the noise and just keep buying. Stay safe out there!

These posts are great! Keep it up!