Market Forecast - Dollar High

Reviewing recent market news and forecasting where the market is headed. Q2 earnings season is starting and the results are likely to disappoint. More selling to come?

This week we’ll discuss an underreported trend of a strong US dollar and rising oil prices double-teaming to wreck havoc in the developing world. This could possibly trigger a global recession.

In other news, despite the eventful past week, the market is still stuck in a stalemate. It’s a tight battle between the bulls and the bears but we think it’s likely to swing in the bears’s favor in the short-term.

For a full discussion on the ongoing economic struggles in the developing world, as well as predictions of where the market is headed, check out the Market Forecast section below.

At a Glance

Falling Euro, Rising Inflation

It was widely reported last week that the Euro and US dollar reached parity for the first time in two decades after the precipitous fall of the Euro in recent months. A weak Euro and soaring energy costs are teaming up to drive up Eurozone inflation.

The European Central Bank is stuck in a rock and a hard place. If they want to fight inflation, they need to raise interest rates, but that will put the EU’s weaker southern economies at risk of defaulting on their debt. If the ECB doesn’t raise interest rates, inflation goes unchecked and the Euro continues to fall against the US dollar, further pushing inflation up as import costs soar.

More on the EU’s economic woes in this Friday’s newsletter issue.

Hot June CPI Report. Have We Reached Peak Inflation?

The Short: June’s CPI report was released last week, and it’s hot. Year-over-year inflation rose to 9.1%. This was higher than the Dow Jones estimate of 8.8% and much higher than May’s print of 8.6%.

The Long: The concerning part of the report is the wide variety of goods categories (e.g. shelter, autos, apparel) that are contributing to inflation, besides just energy and food costs. This indicates that the American consumer’s appetite for spending is still incredibly strong and could signal elevated inflation even if energy and food prices fall.

Interestingly, the market shrugged off the hot inflation report. Expectations rose for a 100-basis-point rate hike after the report but quickly fell when St. Louis Fed President James Bullard said on Friday that he’s hesitant to support such a large hike and still prefers 75 basis points. In addition, economists and analysts are starting to suggest that we’ve reached peak inflation given the recent rapid decline of commodity prices.

OPEC Isn’t Raising Oil Production, Despite Biden’s Visit

The Short: As we predicted, despite Biden’s visit to Saudi Arabia, he would be unable to get OPEC to raise oil production. The official reason from OPEC is that its current oil production rate is already close to capacity, while any new oil production decisions should be made with OPEC+. Awkwardly, Russia is in OPEC+. Since this news, crude oil has rebounded to above $100 per barrel.

The Long: While Biden was mostly rebuffed by OPEC on oil production matters, the Saudis did pledge to raise oil production by more than 1 million barrels per day to over 13 million barrels per day. The problem is, they plan to reach this new output rate in 2027!

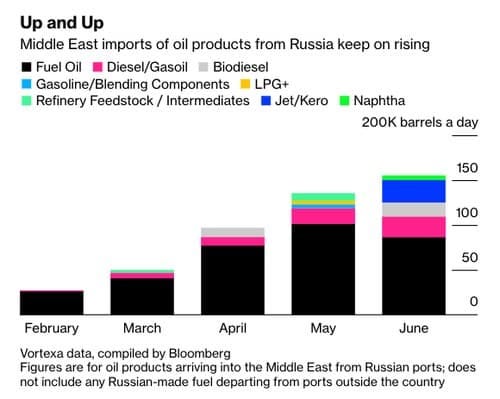

Interestingly, the Middle East has been ramping up oil imports from Russia, with Saudi Arabia doubling Russian oil imports in the second quarter. This has freed up oil for export, thus reducing global oil prices but also contradicting the spirit of US-led sanctions against Russia.

Massive S&P500 Earnings Week

The Short: Following up on the earnings contraction thesis we shared recently (TLDR: it’s Q2 earnings season and there are expectations that earnings will fall, which should push the market lower), this week we’ll have a significant chunk of S&P500 companies reporting earnings. 73 of them, to be exact.

The Long: Last week, a few major banks reported earnings and we’re already seeing the impact of the Fed’s monetary tightening on their bottom lines. Goldman Sachs’s profits fell 47%, Bank of America’s profits fell 32%, and JP Morgan has suspended share buybacks to shore up their balance sheet in anticipation of loan losses.

The question now is whether the rest of the market will also report disappointing earnings. If so, it’s likely that the S&P500 will fall, thus continuing the bear market. We’ll find out soon enough.

Market Forecast

Bad Withdrawal From a Dollar High

How do you bankrupt a country?

One way to do so is to have the country be so used to a cheap US dollar and cheap oil that they start relying heavily on dollar-denominated bonds for funding. Then, block off Russia, the world’s second largest producer of oil, from the global oil market while rapidly raising US interest rates which causes the US dollar to appreciate.

Aside: Dollar-denominated bonds are bonds issued by non-US countries that are paid back in US dollars rather than in domestic currencies. Dollar-denominated bonds are generally more attractive to international investors as they have less foreign exchange risk.

Aside 2: Oil is mostly priced in dollars in the global market and a strong dollar and rising oil prices amplify each other’s effects to make imports for non-US countries significantly more expensive, thus draining their foreign exchange reserves.

A strengthening US dollar makes it much harder for a country with dollar-denominated bonds to acquire dollars to meet payments for outstanding bonds. What’s worse is that the global bond market sees this and starts selling these bonds on fears that they can’t be repaid. This raises interest rates, which makes it more expensive to issue more dollar-denominated bonds to cover existing bond payments.

Since the majority of global trade is denominated in dollars, the sudden removal of dollar liquidity from these countries can destroy their import capacity as they simply cannot afford to import more dollar-denominated goods.

For import-reliant countries, this is disastrous. It’s exactly what’s happening in Sri Lanka. For those that haven’t heard, skyrocketing inflation and a lack of fuel have caused massive protests so intense that the president was forced to flee the country. The protestors even broke into the President’s House.

Many other developing countries (e.g. Panama, Ghana, and Ecuador) that rely on dollar-denominated bonds for funding are also experiencing the same dollar liquidity crunch.

If the US dollar and oil prices continue to rise, several things are likely to happen:

Political revolutions, as seen in Sri Lanka

Falling commodity demand from developing countries, which means lower commodity prices. We are already seeing this happen. Copper’s price has been crashing and is down 35% since four months ago. Wheat is now trading below where it was when the Ukraine war started. Many other commodities are experiencing similar drastic price declines.

Although falling commodity prices helps with lowering inflation, the economic struggles of the developing world can easily spill over to the rest of the world, triggering a global recession.

It’s unfortunate that to cool down inflation in the US, the Federal Reserve’s policy of raising interest rates is implicitly trading away economic stability in the developing world for lower US inflation.

Those hurt the most by this are the regular people living in affected countries loaded with distressed debt. Let’s hope that global markets recover, the US dollar and oil prices fall, and the balance of payments for developing countries are brought back into equilibrium.

Market Forecast

Despite the eventful past week, there are still too many uncertainties to make a long-term market forecast with conviction. However, for the short-term, we think that stocks are likely to go down.

The main impetus for a short-term downwards move is Q2 earnings season, which is just starting. The majority of S&P500 companies are reporting earnings this month and their results will likely disappoint with inflation eating into margins. The earnings of large tech companies, which represent a significant portion of the index because of their size, should also be under pressure as international profits fall due to a strong dollar while advertising profits fall from a contracting advertising market.

The long-term forecast is a lot murkier. As mentioned before, there are just too many unknowns. Although falling commodity prices helps cool inflation, the wildcard for commodity prices is the war in Eastern Europe, which doesn’t seem to be cooling down anytime soon. The situation is volatile and anything could happen. JP Morgan estimates that if Russia cuts its oil production by 5 million barrels per day, global oil prices could soar to $380 per barrel. What’s surprising is that Russia can afford to do this, and likely won’t hesitate if the war starts to go dramatically against their favor.

On the other hand, a sovereign debt crisis in the developing world could trigger a global recession, which is likely to be initially bad for stocks but it will also force the Fed to loosen monetary policy. This can end up being a net positive for US stocks.

To summarize, we expect the markets to fall in the short-term while there are too many uncertainties to make a long-term forecast with conviction.