Market Forecast - Europe Playing Catch Up

Reviewing market happenings this past week as well as what's to come. The macro environment looks grim heading into the second half of the year, but we often don't know how stocks will react.

At a Glance

What happened to FinTech? FinTech’s forward revenue multiples have compressed the most relative to other tech sectors in this bear market. In tight monetary policy conditions, the market seems to be emphasizing the “Fin” over the “Tech”. This has also caused many to realize that the moats of many top FinTech firms are not as strong as people thought.

Europe is playing catch up to the US and tightening monetary policy. The European Central Bank’s (ECB) key interest rate has been at -0.50% since 2019. The bank signalled earlier today that they will likely raise the rate to zero by September, and “could continue raising rates after that”. If they follow through, this would be the first ECB rate hike in 11 years.

Like the US Fed, inflation seems to be getting to the ECB. Germany’s Finance Minister Christian Lindner commented earlier today that inflation is the Eurozone’s biggest worry, and EU members need to reign in spending. Talk about austerity!

The Fed cares about the Job Quits Rate and Unemployed to Job Openings Ratio the most. To predict the Fed, you need to understand what they care about. This weekend I read a paper from the Peterson Institute for International Economics that aligns with Fed Chair Jerome Powell’s rhetoric, and dives into the details.

To summarize, there are three job market indicators most commonly used to predict wage growth: unemployment rate, unemployed to job openings ratio, and quits rate. So far in the pandemic-era, the unemployment rate has been a poor predictor of wage growth while the unemployed to job openings ratio and quits rate have continued to work. Both are what Powell constantly references. If you want to better understand the mindset of the Fed, I encourage reading said paper.

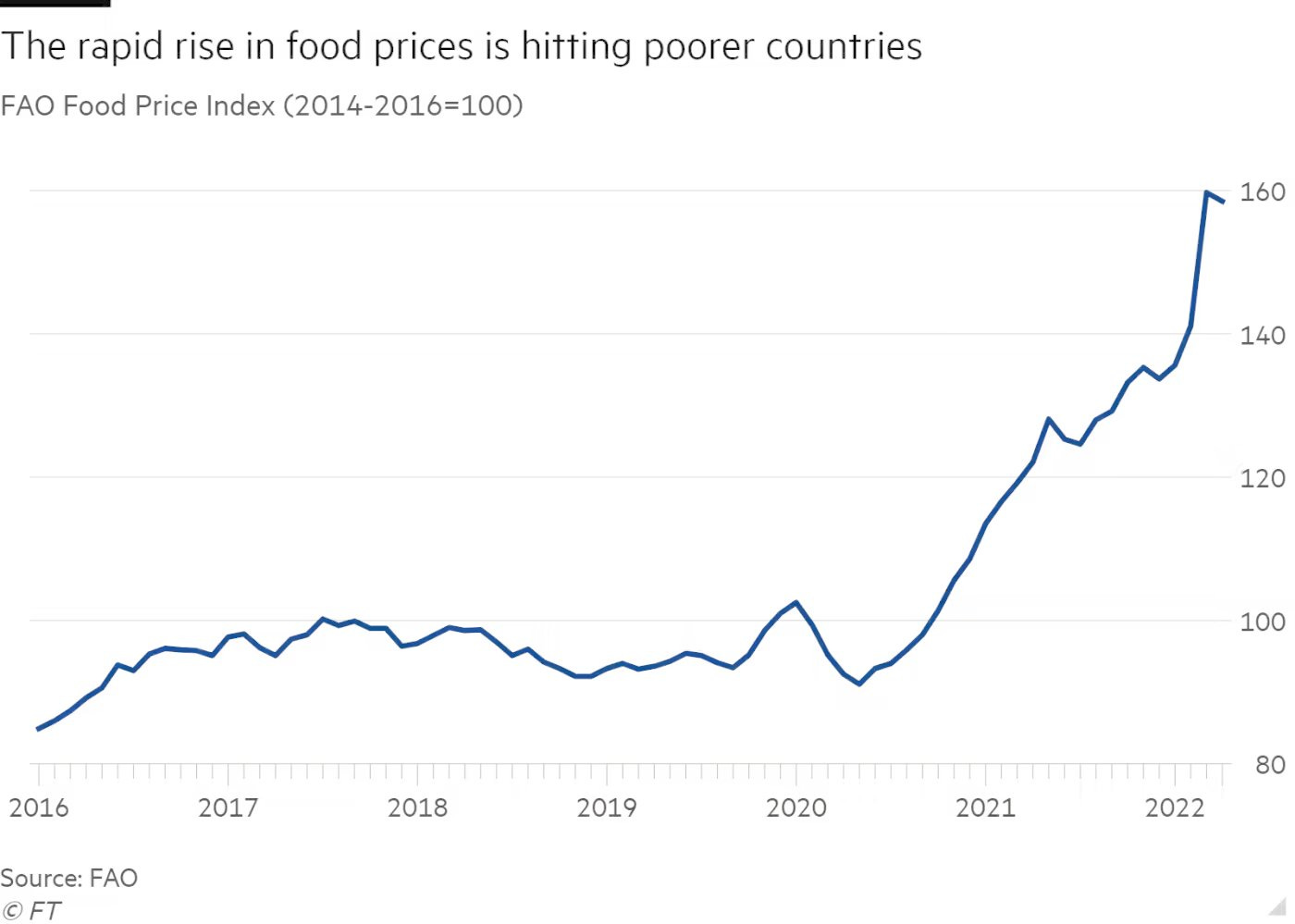

Global food crisis. Europe, Middle East, and Africa first. Last week, UN secretary general António Guterres stated that shortages of grain and fertilizer caused by geopolitical conflicts threaten to “tip tens of millions of people over the edge into food insecurity”. With Europe, and to some extent the world’s, bread basket engulfed in war, we’re starting to see a severe contraction in global food supply. This has caused nations to begin enacting protectionist food export policies, with India banning wheat exports and Indonesia banning palm oil exports. In addition, soaring food prices have started to cause unrest in some parts of the world. Last week, nationwide protests erupted in Iran over soaring food prices.

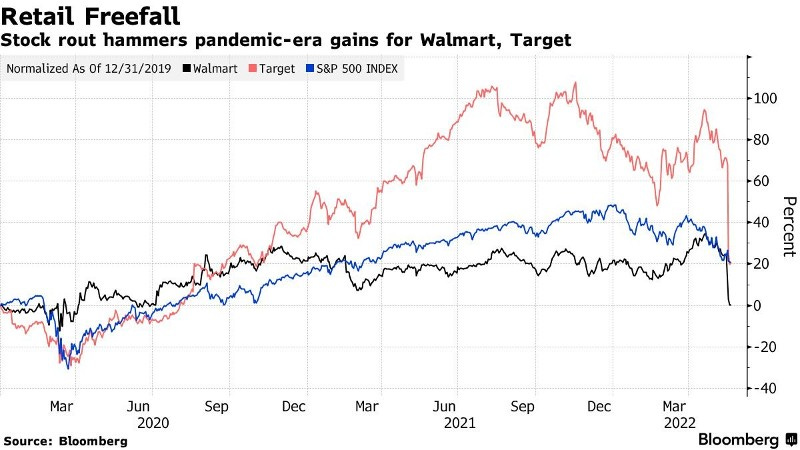

Inflation cuts into Walmart and Target’s earnings. Last week, Walmart and Target reported earnings that the market found disappointing. Soaring food and fuel costs as well as inventory write-downs are cutting into the earnings of both retailers. It’s only a matter of time before both need to pass the costs on to the consumer to save their own earnings.

The Forecast

As for the market forecast, we don’t see it changing as much from last Friday’s market forecast.

In short, we’re watching out for the Fed to start unwinding its balancing sheet on June 1st (next Wednesday), the BlackRock Momentum ETF’s rebalancing from tech to energy this week, as well as important inflation-related economic numbers being reported on Friday (April PCE and Core PCE inflation, real and nominal consumer spending, real and nominal disposable income). As mentioned last week, we think that there will be elevated volatility as we approach the end of the week.

Zooming out, the macro situation for the latter half of the year might look pretty grim but we shouldn’t let that sentiment dominate our trading plans. We often don’t know how stocks will react even if we have a good sense of where macro is headed, especially if the Fed decides to ease off on the brakes.

Let’s end this issue with some positive news. The 10-year treasury yield is forming a head and shoulders pattern, which if you think technical analysis holds weight, suggests that the yield will fall in the near future. A lower yield will ease off pressures on the stock market.