Market Forecast - I Was Wrong

Reviewing market happenings this past week as well as what's to come. This week, I discuss how important energy prices are to inflation right now.

At a Glance

I Was Wrong About Inflation

I was wrong about inflation. Last year I wrote two articles titled “Inflation Is Not Here to Stay” and “The Only Guide to COVID Inflation You'll Need”. Both claimed that inflation is transitory. It’s clear today that we’re in a unique environment that we haven’t seen in a couple decades where inflation is rearing it’s menacing face again after a prolonged period of deflation. Although, to be fair, a large part of the inflation is driven by an energy supply crunch and supply chain pressures from geopolitical events that one couldn’t really predict at the time those articles were published, a lot of it is also coming from rising wages and a continuously strong and growing US consumer base, which I incorrectly discounted.

Predicting macroeconomics is hard and you will be inevitably wrong. As a trader/investor, you need to constantly revisit your assumptions, especially when things are changing so quickly in this chaotic world.

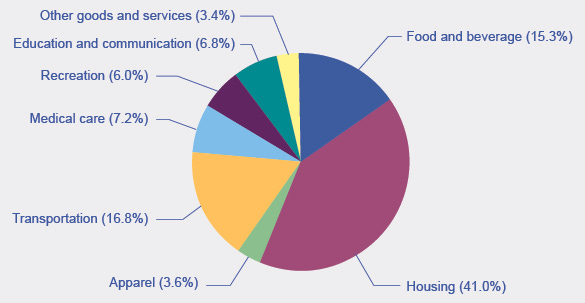

The May CPI Report Was Bad

The Short: Last week, the May CPI report was released and it crushed the expectations of market bulls hopeful of inflation peaking and a September slowdown in Fed rate hikes.

The Long: Both the headline and core CPI numbers (minus energy and food) were higher than expected. Headline CPI came in at 8.6%, higher than an estimated 8.3%. Core CPI came in at 6.0%, higher than an estimated 5.9%. Not surprisingly, the headline CPI is being driven by soaring energy and food prices, while core CPI is being driven by shelter, airfares, and used cars and trucks. The shelter component accounts for about a one-third weighting in the CPI and is rising as a latent effect of the red hot real estate market of the prior year. Many market participants were hopeful of inflation peaking in the summer, allowing the Fed to slow down its tightening in the fall. Last week’s CPI report proved them wrong.

Fed Meeting This Week

The Short: June’s FOMC meeting will be held this week, with results released on Wednesday. The market is expecting the Fed to be a lot more hawkish in its tone given the recent CPI report. Some are even expecting a 75 basis point hike rather than the prior consensus of a 50 basis point hike.

The Long: Some elements of the Fed might have been in the same camp as market bulls and were expecting inflation to peak in the summer. For example, the Altanta Fed President Raphael Bostic had suggested a slowdown in rate hikes in September a few weeks ago. The recent CPI report should decisively align Fed members towards more aggressive tightening moving forward. The report was so worrying that some (e.g. Barclays) are predicting the Fed will go for a 75 basis point hike this meeting. The last FOMC meeting’s 50 basis point hike was the largest one-time hike in 22 years and now people are expecting a 75 basis point hike! Regardless of the size of the next hike, expect Powell’s press conference rhetoric to be incredibly hawkish.

Building a Rocket Company is Hard

The Short: Astra’s launch of its LV0010 rocket carrying two satellites on NASA’s TROPICS-1 mission failed to reach orbit. This is the company’s second failure in three launches this year and could doom the company’s prospects.

The Long: Astra is a manufacturer of small rockets that went public through a SPAC. They are a relatively young rocket company that aims to carve out a market niche for small rockets that can be quickly manufactured and launched from almost anywhere in the world. It’s clear after this year’s performance of Astra’s rockets that their technology is far from ready. Unfortunately, they might not have enough funding to last through this bear market, with their SPAC deal only raising $500 million. Building a rocket business is expensive. Expect Astra to look to be acquired by another space company.

Market Forecast

Energy is Key

It feels like inflation hinges on energy prices right now. Although you can minimize the effects of energy prices by focusing on core CPI, it still affects the prices of goods and services across all categories. Stuff needs to be made and transported, which requires oil, diesel, and jet fuel. High energy prices are also why many are worried about a possible stagflationary situation, where growth stalls but prices continue to rise (everyone’s paying extra for energy, but not actually buying more stuff).

To this end, Biden has finally reneged on his vow when he entered office to make Saudi Arabia a “pariah” over the killing of Saudi Arabian journalist Jamal Khashoggi. Biden is expected to travel to Saudi Arabia next month and meet face-to-face with the kingdom’s de facto ruler Mohammed bin Salman (MBS) in an effort to reset relations and hopefully get OPEC to increase oil production and alleviate oil prices. This was something the Biden administration has largely tried to avoid, but desperate times call for desperate measures.

It’s interesting to note that since 2018, the United States has been the world’s largest producer of oil and natural gas, yet underinvestment and heavy regulation in the country’s energy infrastructure has prevented the country’s abundance of energy resources from making a meaningful dent in domestic energy prices.

As such, for a meaningful reduction in inflation, we’d want to see energy prices fall and that hinges on two things right now: (1) the Russia-Ukraine war subsiding and the re-accepting of Russian oil in the Western world (2) the success of Biden in appeasing MBS to the degree that MBS is willing to get OPEC to raise oil production.

Short of the fall of energy prices, we’re likely to dip into a stagflationary environment where inflation from energy costs is further egged on by rising wages and rising shelter costs.

A Quick Word on Stocks

As for stocks, we’re likely to see stock prices decline further as the market has yet to price in a broad-based fall in earnings that many are expecting in the second half of the year. Many analysts have not reduced their earnings expectations and the S&P500 is still trading at a forward earnings multiple close to its pre-pandemic peak.

Outlook

Needless to say, the market’s outlook is bleak. The best approach to take in times like these is to keep dollar cost averaging into deeply discounted stocks. You’d be well rewarded when the market inevitably recovers and stabilizes.