Market Forecast - Lessons Learned

Reviewing recent market news and forecasting where the market is headed. This week, we'll review two lessons learned from recent market movements and share predictions for the second half of the year.

Apologies for last week’s impromptu hiatus in publishing newsletter issues. Three issues every week can take a toll and we needed a break to recuperate, recenter, and come back stronger.

To start the week off strong, we will be donating to the Cancer Research Institute. The CRI funds the development of immunotherapies for cancer, from lab to clinic to cure. 88 cents of every donated dollar goes to cancer research programs.

As before, don’t feel pressured to join us, we simply ask that we all do a little extra good this month, whether for a cause you believe in, a friend, a loved one, or even for yourself.

In this week’s Market Forecast issue, let’s talk about two major lessons learned from the past year’s surge in inflation and the recent market rally. We’ll end the issue by sharing where we think the markets are headed in the second half of the year. For the full discussion, check out the Market Forecast section below.

At a Glance

The Market Rally Continues

The market rally that started right after June’s Federal Open Market Committee (FOMC) meeting (where the Federal Reserve raised rates by 0.75%, the largest in a single meeting since 1994) continued in strength last week. This was fueled by better than expected Q2 earnings results and cooling inflation.

The market is now up more than 16% off its June lows of around $365!

Oil Down Again

The Short: The price of WTI crude oil fell by a little more than 5% today to under $88 a barrel at the day’s lows. This is its lowest price since January.

The Long: Soaring energy prices have been a major source of inflation in the past few months and falling oil prices is another sign of cooling inflation. This morning’s price drop came after China released weaker than expected economic data for July. Oil’s price has recently been buoyed by expectations of China’s economy rebounding with lockdowns easing. Unfortunately, this anticipated economic rebound is off to a slow start.

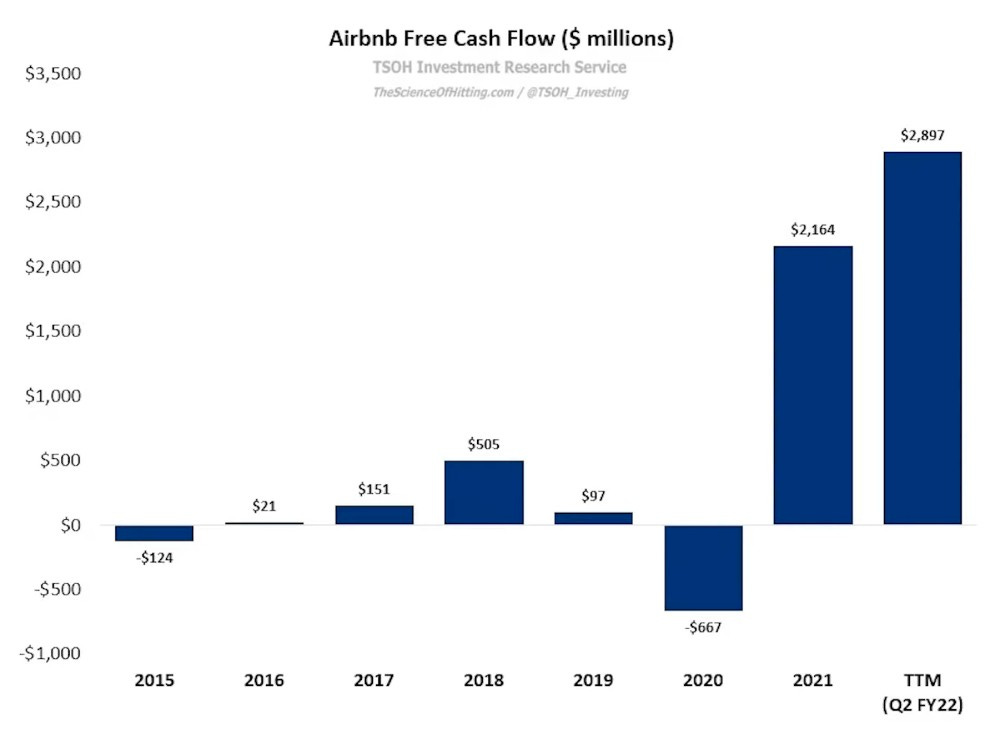

Free Cash Flow

The Short: High inflation and tightening monetary policy have caused the market to value Free Cash Flow over “Growth At All Costs”. Many companies have swiftly responded to the new modus operandi.

The Long: Uber CEO Dara Khosrowshahi unintentionally sent an early signal of this major market sea change through a leaked company letter in May where he stated: “After earnings, I spent several days meeting investors in New York and Boston. It’s clear that the market is experiencing a seismic shift and we need to react accordingly… In times of uncertainty, investors look for safety… Now it’s about free cash flow. We can (and should) get there fast.” Uber reported its first ever positive free cash flow quarter in Q2 2022.

One chart that exemplifies this major market sea change is Airbnb’s trailing twelve months free cash flow, which shows a significant shift in the company’s operating priorities towards generating free cash flow.

Google Layoffs?

The Short: Business Insider recently released an alleged leaked email from Google Cloud’s sales leadership stating that if productivity doesn’t improve, “there will be blood on the streets”.

The Long: This alleged threatening email from Google Cloud’s sales leadership follows on the heels of Sundar Pichai telling Google employees at an all-hands meeting earlier in the month that there are concerns “productivity as a whole is not where it needs to be for the headcount we have”. The Insider report also revealed that Google had quietly extended a hiring freeze that was originally intended to be two weeks long.

Although Google’s stock price staged a strong rally after its recent Q2 2022 earnings call, the results were far from positive with many missed expectations and key business units like YouTube and Google Cloud experiencing slowing growth.

Market Forecast

Two Lessons Learned

Let’s discuss two major lessons learned from the past year’s surge in inflation and the recent market rally.

First, although inflation is painful for the entire economy, it’s especially painful for low income earners and less noticeable for high income earners. As such, businesses that serve consumers from the former segment do poorly in an inflationary environment, while businesses that serve the latter perform better. This dichotomy is exemplified by the stark difference in business results between Six Flags theme parks and Disney theme parks. While traffic to Six Flags theme parks has been lackluster despite the economy reopening, Disney theme parks have been thriving. Six Flags’s Q2 revenue fell 5% year-over-year from $460 million to $435 million while Disney’s theme parks saw its Q2 revenue increase by 72% year-over-year from $4.3 billion to $7.4 billion.

The second lesson is that inflationary effects on the consumer are lagging, especially if the consumer has significant excess savings. The market’s mis-prediction of this lagging effect is partly behind the strength of the recent market rally. Many investors expected Q2 earnings results to be “disastrous” as inflation forced consumers to pull back spending. As such, they had overly pessimistic market positions heading into Q2 earnings season. However, American consumers had so much excess savings (over $2 trillion at the start of 2022) that the adverse impact of inflation on spending was muted and earnings results were Bad But Not That Bad. This forced the aforementioned overly pessimistic market positions to be unwound (i.e. shorts covering, redeploying of cash), thus helping to propel the market upwards.

The above thesis is supported by data from GS Prime (Goldman Sachs’s Prime Brokerage division) showing that the third largest institutional short covering event in the past decade happened in the past month.

Too Early to Celebrate?

The market has recently been relentlessly marching upwards but perhaps it’s too early to celebrate the end of the 2022 bear market.

There are two primary reasons for this.

First, inflation at 8.5% is still far above the Fed’s target level of 2%. Despite signs of cooling inflation, there’s historical precedence of a Fed that was too eager to loosen monetary policy resulting in inflation resurging (during the tenure of infamous Fed chair Arthur Burns). Jerome Powell is well aware of this and wants to avoid making the same mistake, lest he ends up tarnishing his legacy. As such, the market may be too optimistic and the Fed is likely to keep its foot on the brakes for a lot longer than many expect. This sentiment was shared by former NY Fed President William Dudley in a recent CNBC interview.

Second, the lagging effect of inflation on the American consumer (as discussed above) means that we might only see inflation’s real impact on consumer spending in the latter half of the year. The market’s overly pessimistic positioning prior to Q2 earnings season need not be wrong, just early.

Moving forward, the strength and extended duration of the recent market rally paired with a continued pessimistic economic outlook suggests that there will be more down than up in the coming months. At this point in time, we think it’s better to keep risk low.