Market Forecast - The Only Thing That Matters

Reviewing market happenings this past week as well as what's to come. This week, I discuss the only thing that matters in the market right now.

At a Glance

Are We in a Bear Market Rally?

This is the key question right now. Last week, we went from a $386 Snapchat bottom to a roaring $415 high by the end of Friday. In The Forecast section below, I share my thoughts on whether we’re in a bear market bottom or not, and what I believe is the only thing that matters to this market right now.

Inflation Might Be Cooling

The Short: Last week, the core Personal Consumption Expenditures Price Index (core PCE index) for April was reported. The index rose 4.9% year-over-year and 0.2% month-over-month. This is less than the 5.2% yoy and 0.9% mom numbers of March and was well received by the market.

The Long: The core PCE index is often considered the Fed’s favorite inflation measure since it excludes food and energy, two goods categories heavily affected by international conditions that are out of the Fed’s control. The market clearly liked April’s PCE numbers and bounced hard from Tuesday’s low of $386 to end the week at over $415. However, these numbers are still way above the Fed’s 2% annual inflation target and we’ll need continued signs of cooling from top inflation indicators to remain bullish.

Fed Signals Slowdown in Interest Rate Hikes

The Short: Atlanta Fed President Bostic said on Monday that the Fed was open to slowing down rate hikes in September after two 50-basis-point hikes in June and July. The market expected three 50-basis-point hikes in June, July, and September but now expects September’s hike to just be 25 basis points. This was the canary in the coal mine for the market rally in the second half of the week.

The Long: Investors were expecting the Fed to aggressively raise rates well into September. Bostic’s comments on a September rate hike slowdown, in combination with weakening core PCE index numbers, helped to build a strong case that the Fed will ease off on the brakes in the fourth quarter. The market now expects two 50-basis-point hikes in June and July, followed by a 25-basis-point hike in September when it used to expect three straight 50-basis-point hikes.

The chart below is important. It’s the historical market expectation for where interest rates will at least be by September 21st, courtesy of the CME. Over the last week, there’s been a significant drop in expectations for the rate to be at 2.25-2.5% by September (three straight 50 basis point hikes) but the probability for a 2.0-2.25% rate (two 50 basis point hikes and a 25 basis point hike) remains the same. This lowering of interest rate hike expectations definitely helped fuel last week’s massive stock market rally.

More Important Inflation Numbers Reported Later This Week

The Short: Several important labor market numbers for April will be reported later this week. Total Job Openings and the Quits Rate are reported on Wednesday while the Unemployment Rate, Average Hourly Earnings, and the Prime-Age Labor-Force Participation Rate are reported on Friday.

The Long: The Fed is closely watching the labor market as a leading indicator for inflation. They are most scared of a Wage-Price Spiral, which is driven primarily by tight labor market conditions. The labor market has been exceptionally tight in the past year and continued tightness dampens hope of the Fed slowing down its monetary tightening policies. The key numbers to watch for this week are the Job Openings to Unemployed Ratio and the Quits Rate. Jerome Powell has hinted that he cares most about these two labor market measures.

The Fed Starts Selling Off Its Balance Sheet On Wednesday

The Short: As I’ve mentioned in previous newsletter issues, the Fed starts selling off its $7 trillion balance sheet on Wednesday. They will sell off up to $30 billion in Treasuries a month and up to $17.5 billion in Mortgage-Backed Securities a month. After three months, these caps will double to $60 billion in Treasuries and $35 billion in Mortgage-Backed Securities. The market is worried.

The Long: Historically, when the Fed sold off its balance sheet, the market has wobbled. The best example of this is in Q4 2018 when overnight repo rates shot up and the stock market crashed. This ultimately forced the Fed to reverse its balance sheet sell-off and interest rate hikes. We don’t know how well this upcoming sell-off cycle will go but there’s definitely a backdrop of worry regarding its effects. This will be, in absolute terms, the largest sell-off of assets from the Fed’s balance sheet in history.

The Forecast

I’ll get right to it. The only thing that matters to the market right now is what the Fed thinks domestic inflation is like and its expected policy response. Nothing else matters as much as this. The talking heads on CNBC, pundits on fintwit, and authors on Bloomberg might talk about a possible recession, commodity prices, supply chain problems, etc. etc. but dare I say that these are mostly just noise. The market will move based on what it thinks the Fed will do.

Last week is a great example of this when a minor suggestion from the Fed of a September rate hike slowdown triggered a massive rally. Another great example is in March 2020 when the market embarked on a raging bull cycle after the Fed opened the floodgates for easy money… even as the country was in lockdown, plunged into a recession, and millions of people lost their jobs.

Every short and medium-term stock market move hinges on the Fed.

As such, to play this market we need to watch the Fed closely, and understand what it cares about.

Last week’s September rate hike slowdown comments by Altanta Fed President Bostic was a signal for a market rally in the latter half of the week. The Fed will no doubt lay more breadcrumbs in the future that can drastically change what the market thinks the Fed will do. We need to pay close attention for these breadcrumbs.

We also know that the Fed is focused on the labor market and uses labor market tightness as its best leading indicator for inflation. The Fed considers the Job Openings to Unemployed Ratio and the Quits Rate as the most important measures of the labor market where inflation is concerned. Both were heavily cited by Jerome Powell in the last FOMC press conference.

It’s unclear where the market is headed this week, but the labor market numbers released later in the week will definitely set the tone. Signs of cooling off will serve as more fuel for the ongoing rally while continued tightness can plunge us back down, making last week’s rally yet another bear market bounce.

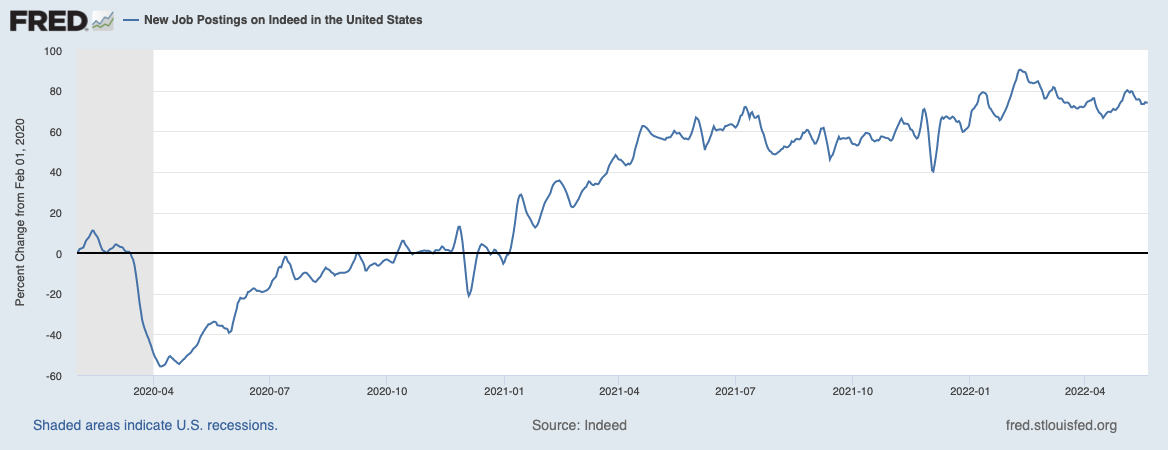

How Does One Get Labor Market Numbers Faster?

Labor market numbers are released weekly (Initial Jobless Claims, Continuing Jobless Claims) and monthly (Job Openings, Quits Rate, Unemployment etc.) but this cadence might be too slow for traders that want to front-run the Fed. Thankfully there are lesser known labor market metrics that are updated daily from Indeed which even the Fed tracks closely. The graphs below are from the St. Louis Fed containing daily new job openings and total job openings on Indeed.

If you’re looking to get ahead of labor market reports, this data from the St. Louis Fed will certainly be helpful.

Swimming With Rebalancing Whales!

If you missed it, here’s last week’s research article on how Target Date Funds might be responsible for reversing market corrections at the end of quarters. I think you’ll find this an interesting and informative read!