Research - Avoid Volatility, Beat Market By 4x

We show how a volatility managed strategy put forth by an academic paper "Volatility Managed Portfolios" significantly outperformed the market by more than 4x.

In this post, we will explore the volatility managed strategy put forth by ALAN MOREIRA, TYLER MUIR in their 2017 paper Volatility Managed Portfolios. My results show that following their methodology for a little over the past decade would have significantly outperformed the market. Specifically, starting from 2010, the volatility managed strategy saw a total return that was more than four times greater than the buy and hold strategy. Put in other words, $100 invested in said strategy in 2010 would have turned into more than $1700 today, while $100 invested in a buy and hold strategy would have turned into just $480. Even better, this strategy appears to be relatively accessible to a retail trader through the ETFs: SPY, UPRO, & VGSH.

TLDR and How Do I Replicate?

The general idea behind the strategy is to weave in and out of SPY (ETF for the S&P 500) based on market volatility. If the market is volatile, we stay in safe US government bonds (VGSH, ETF for short term US treasuries), and if the market is calm, we buy into SPY with leverage.

The reason this works is that the US stock market generally goes up, especially in low volatility periods, and low volatility also significantly reduces the cost of leverage.

We can measure market volatility by calculating the recent variance of the price of SPY.

Here’s a high level summary of the process:

If the variance of SPY is below a certain threshold (low volatility):

Invest in SPY with leverage

If the variance of SPY is above a certain threshold (high volatility):

Invest in safe US government bonds

For more specific instructions on replicating this strategy, see the Detailed Steps to Replicate section below. In the following sections, we also dive into the theory behind this strategy and describe how we verified it by performing a backtest.

Understanding Why This Works (Deep Dive)

Moreira and Muir’s hypothesis

In their paper, Moreira & Muir suggest that over the past ~100 years, investors would have been able to achieve positive alpha in their portfolio by regularly adjusting their equity exposure as realized volatility fluctuates. In their paper they define their methodology as follows:

Where:

ft+1 is the buy and hold portfolio’s excess return

σ squared is the realized variance over the past month

And c is a constant used to control the average exposure of the portfolio

They further postulate that at any given time, the optimal portfolio weighting is proportional to the attractiveness of the risk return trade-off.

Using these formulas, they suggest that each month an investor should look to reassess their current equity exposure based on the realized variance from the previous month and re-adjust accordingly.

To get an idea for what all this means in practice, we can look at the portfolio weights that were used in my backtest.

The y-axis is the proportion of the portfolio we allocate in each asset (SPY vs VGSH). The blue line is the proportion in SPY and the yellow line is the proportion in VGSH. When the total proportion is above 1.0, the portfolio is leveraged.

What can be seen above is that this strategy usually maintains a healthy amount of leverage when invested in SPY, but will quickly shift into VGSH (safe government bonds) when volatility spikes to remain there until volatility subsides.

For instance, you can see that this strategy shifted exposure (almost entirely) into VGSH at the beginning of the COVID-19 pandemic. It remained there until around June before returning to its normal leveraged position which allowed it to take advantage of the bull run that occurred in the back half of that year.

Muir & Moreira’s explanation for why this works to generate excess returns is that: “variance is highly forecastable at short horizons, and… only weakly related to future returns.”

Does It Work in Practice? (Backtest)

Below we explore how this strategy would have performed in the past few years, but before we get into that I’ll give you a little more information about the values I used for some of the variables from above.

For my backtests, I used the following values for c and ft+1:

For c, I used the square of the median VIX value (as a percent) since 1990 (~0.031)

For ft+1, I used the average annual return for S&P 500 minus the 2-year treasuries yield (10.5% - risk free rate)

Also, to give us something to compare the performance against, I also backtested the following hypothetical portfolios:

A buy and hold portfolio that is 100% exposed to SPY

An 80:20 portfolio that maintains an 80% exposure to SPY and a 20% exposure to VGSH.

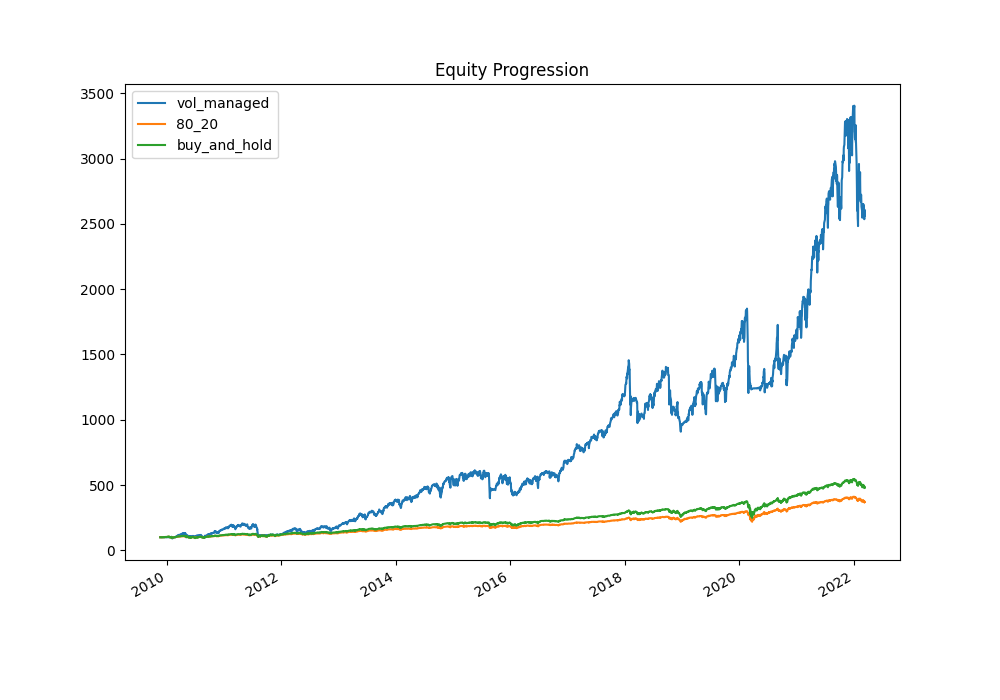

Below you can see the returns generated by each of these example portfolios:

As you can see the “Volatility Managed Portfolio” clearly outperformed the other two over this time period.

Some of the noteworthy observations about the “Volatility Managed Portfolio” are:

It beat the “Buy and Hold” CAGR by ~1656 bps (portfolio would be 5x larger in 10 years!)

It had a higher Daily Sharpe ratio than both the Buy and Hold and the 80:20

It had an alpha of ~0.008 over the buy and hold portfolio.

However, these results are idealized as the backtest does not need to pay any premiums on borrowed money and has no leverage constraints, and as such aren’t indicative of what could actually be accomplished by your average investor. That said, there are low cost leverage options available to most investors via leveraged ETFs which can be used to obtain similar results. Next we will show how the desired leverage can be obtained through a combination of SPY and UPRO and compare that portfolio with the above.

Detailed Steps to Replicate

The average retail investor will have limited access to margin trading through their brokerage. Generally speaking they will be limited to 2x exposure (i.e. double your money from borrowing), and will need to pay high interest on the money borrowed while they maintain the position. For instance, E*TRADE offers margin at >= 7.2% for any account under $500K.

However, a simple work around to getting cheap leverage is available through easily accessible leveraged ETFs such as UPRO.

First lets go over the ETFs that will be used by this strategy:

SPY: This is an ETF that is commonly used to gain S&P 500 exposure. It holds all of the assets included in the index weighted by their respective market caps

UPRO: This is a 3x leveraged ETF for the S&P 500

VGSH: This is an ETF used to gain exposure into the US treasury bond market. It holds various bonds that have an average maturity of 2 years.

By combining these 3 ETFs we are able to reasonably replicate the strategy.

The key to this strategy is calculating a value we’ll call wt+1 (see formula above), which tells us how much leverage we should use to invest in the SPY or whether we need to be in safe US government bonds. If wt+1 is above 1, we’re invested in SPY with leverage. If wt+1 is below 1, we are invested in a mix of SPY and US government bonds with no leverage.

Let’s dive into the specific steps to replicate this strategy:

Choose a c value that will be used for the calculation

This value will control the average leverage taken on by the strategy

Calculate the past month’s daily log returns for SPY

Calculate the annualized variance of the daily log returns

Calculate the expected excess returns of SPY by subtracting the current “risk free rate” from the average annual returns

Scale the excess returns using our formula for ft+1 above (i.e multiply the excess returns by the fraction of c over the realized variance)

Divide the scaled returns by the realized variance to find our wt+1

If wt+1 is > 3 set it to 3 since that is the most leverage we are able to obtain via UPRO

For any wt+1 value above 1 the following equations can be used to find the equivalent SPY and UPRO exposures respectively:

For any wt+1 value under 1 a combination of SPY and VGSH can be used.

Having obtained wt+1 we can determine our allocation into SPY / UPRO / VGSH. We will assume that the investor seeks to invest $1000

If the value for wt+1 is > 1 (e.g 1.5):

Determine UPRO exposure using the formula from above. (1.5 - 1) / 2 = 25%

An investment of $250 is then made into UPRO

SPY receives the remaining allocation of $750

If the value for wt+1 were less than 1 (e.g 0.75):

75% would be allocated to SPY (i.e. $750)

The rest would be invested in VGSH (i.e. $250)

This process would be repeated each month as volatility fluctuates.

As mentioned above, we backtested this practical ETF-based strategy and found that it does a reasonable job of replicating the theoretical strategy, only underperforming slightly.

Conclusions

Overall I would say the backtest seems to suggest that Muir & Moreira’s findings hold weight, and the strategy proposed in their paper seems to be replicable for a retail investor seeking larger returns.

However, anyone considering this strategy should understand the risks associated with using leverage in their trading. I will point out that in my backtest the ETF strategy saw a 47% drawdown on its worst trading day, so anyone attempting to replicate it should consider their appetite for such volatility. Also, any of the figures shown in this post are only relevant to the time period between 11/2009–3/2022 and may not be indicative of future results.