Research - Fixing Netflix

Netflix's stock fell 70% since its all time high just five months ago. What went wrong, and what can we learn from the company's plight?

Netflix’s story so far can be introduced with these two images:

Two consecutive earnings reports, two consecutive massive gap downs.

Analysts were quite bullish going into these two earnings reports and seemed to be caught incredibly off-guard by the two reports.

Perhaps the best embodiment of analysts and investors caught off-guard with Netflix’s stock price collapse over the past few months is Bill Ackman. After the company’s Q4 2021 earnings report in which the stock gapped down almost 20%, Ackman, via a tour de force of a tweet, singlehandedly moved the stock up one hundred dollars or 27% from $360 to $460. He lauded the company and declared that he had unwound more than a billion dollars in interest rate hedges to buy NFLX (unfortunately, to add insult to injury, those hedges would’ve paid off handsomely if he held on for a couple more months).

In a shareholder letter linked in the tweet, Ackman shared his reasons for jumping into the investment.

Netflix’s business has highly favorable characteristics which include:

its subscription-based, highly recurring revenues, which have enormous future growth potential

a truly best-in-class management team and unique high-performance culture (consider Netflix’s remarkable pivot from DVD rental by mail, to video streaming, to becoming one of the greatest producers of beloved content ever)

pricing power derived from the enormous value it delivers to consumers compared with other alternatives

substantial margin expansion, with the opportunity for continued improvement due to economies of scale and the company’s rapidly growing, global subscriber base

an improving free cash flow profile which should allow for continued investments in growth as well as the return of cash to shareholders

For a brief moment after the tweet, Ackman was sitting pretty with Netflix’s stock price increasing by an impressive 27% in just three days. Then the stock proceeded to fall back down to where it landed after the prior earnings report and traded in a range between three and four hundred dollars for the next three months.

Then the Q1 2022 earnings report came out, and it was revealed that the company had lost 200,000 subscribers, which was a far-cry from the company’s own estimate of gaining 2.5 million subscribers. In addition, a drop of another 2 million subscribers was forecasted for the second quarter.

After this earnings report, Ackman licked his wounds and sent a letter to his shareholders letting them know that he sold the Netflix stake, with some estimating it cost his fund $400 million.

Just like Ackman, many analysts and investors were caught up in the bullish story of Netflix, and didn’t see the looming abyss that the stock would soon find itself falling into.

Let’s examine why the market was largely caught offside, what went wrong with Netflix, and draw lessons from this debacle.

Top Stock of the Decade

Perhaps the biggest reason for the market’s overly optimistic sentiment of Netflix is the stock’s tailwind as it came out of the prior decade. For example, CNBC reported in 2019 that Netflix was one of the best stocks of the decade, “delivering a more than 4,000% return”.

Netflix pioneered the experience of unlimited and on-demand premium content streaming, accessed through a simple monthly paid subscription. Compared to a world where content was expensive and inconvenient to purchase (cable subscriptions, per-per-view, DVD and Bluray), Netflix was an extraordinary experience and gave hope for a bright future of media consumption. Everyone loved the service. Netflix quickly became a household name and found its way into popular vernacular. Was it “buy NFLX and chill”? At least that’s what Wall Street was saying.

The market’s optimism for Netflix can be measured with its highly inflated Price-to-Earnings ratio (PE ratio) of over 50 in the past decade, even reaching above 400 twice in 2013 and 2015. In contrast, other FAANG companies traded at much lower PE ratios. Even with Netflix’s recent stock price decline, its PE ratio is still at a respectable 19, slightly below Alphabet’s 21 and way above Facebook’s 13.

Netflix’s Troubles

Leaky Patch for a Leaky Bucket

The main problem with Netflix that many overlooked is the fact that it doesn’t have much of a moat. This allowed looming competition to scale up quickly to chip away and even break off major swathes of Netflix’s unprotected fiefdom.

While everyone was celebrating Netflix’s great experience and massive growth in the early 2010’s, major competition was also brewing. Here are some examples of the launches of competing subscription streaming services in the past decade:

HBO Max (launched in 2020)

NBC Peacock (launched in 2020)

YouTube Premium (launched in 2014)

Global expansion of Prime Video (launched in 2016)

Apple TV+ (launched in 2019)

Paramount+ (launched in 2014)

Disney+ (launched in 2019)

It seems like almost every major production company was creating their own subscription streaming service and pulling content away from Netflix. Add into the mix a few big tech companies as well.

Netflix doesn’t have any competitive advantage when subscribers have a wide range of of other streaming services offering a similar viewing experience to switch to. With exclusive content on each platform, a subscriber could jump from service to service, watching what they fancied at the moment. Netflix had a major leaky bucket.

To management’s credit, they saw the impending competition early on and tried to get ahead of it by turning Netflix into its own production company. The company’s original programming division was launched in 2013 and swiftly invested billions into producing exclusive content. The endeavor was quite successful, spawning hit shows like Stranger Things, Ozark, Squid Game, and Arcane.

However, for every hit show or film that Netflix produced, the competition would produce or take away ten other pieces of valuable content.

It’s clear that Netflix’s production arm was not going to scale to create any meaningful moat. It was just a leaky patch for the leaky bucket.

Lack of a Long-Term Strategy: Saturation and Gaming

Although I feel that Netflix’s lack of a moat was the major problem with its business model, I should also mention the supporting cast in this grand plot.

Another weakness with Netflix’s business model is its inability to scale revenue with watch time. A user that spends ten hours a day on Netflix pays the same as a user that spends one hour. This eventually means that Netflix will hit a subscriber saturation ceiling and growth will aggressively peter out as it nears this ceiling. This is exactly what the company is currently experiencing in the US and Europe. Netflix was able to stave off growth concerns from saturation with international expansion, but that will also near a ceiling sooner or later. Unless Netflix finds a new source of subscriber growth in the Martians or Saturnians, they need a plan to scale revenue based on watch time. However, this seems to be a gaping hole in the long-term strategy put forth by the company so far. They can’t kick the can down the road forever.

Instead of solving this problem, the company has decided to pivot to gaming as a long-term strategy. This seems like a misguided path, given how game streaming as a business has failed for so many companies so far, Google being its latest victim. Google launched its game streaming subscription service called Stadia in 2019 with a massive marketing push. However, it never caught on and Google has spent the past year scaling back Stadia, with many high-level Stadia executives jumping ship in the process. If even Google, with its access to vast amounts of money and technical prowess, cannot create a viable game streaming business, what hope does Netflix have?

Fixing Netflix

To fix Netflix, the company can take a page out of the book of another video streaming juggernaut. I’m talking about YouTube. Almost every weakness in Netflix’s business model, YouTube is good at.

Whilst Netflix is facing a leaky bucket in terms of content, YouTube has a major moat around content, being the only platform where independent creators want to upload mid-to-long-form videos to in the West. Because anyone can upload to YouTube, its content library is vast, organic, and self-expanding, appealing to all kinds of cultures, preferences, and trends. The only cost to maintaining this content is the technical cost.

Whilst Netflix can’t scale revenue with watch time (thus facing a subscriber saturation problem), YouTube is able to do so via a highly integrated and optimized ad system. In fact, YouTube’s ad business is so strong that its ad revenue alone in Q4 2021 was larger than Netflix’s total revenue.

Knowing this, how can we fix Netflix?

Netflix should compete with YouTube for independent content creators. Some might argue that this is a futile endeavor given YouTube’s deep roots in the User-Generated Content (UGC) content business and strong moat but even in the strongest moats there are leaks. Many of YouTube’s highest quality creators have been unsatisfied with how the platform is run and are increasingly worried with their precarious “all eggs in one basket” position on the platform. For example, if YouTube decides to ban a creator for whatever reason, they have nowhere else to turn to given YouTube’s monopolistic dominance. As such, a few of YouTube’s top creators have collaborated to create their own video streaming platform called Nebula where they have more creative freedom and are able to publish extended or more premium versions of their content.

Netflix should take advantage of this organic demand for a separate platform that competes with YouTube. This budding need of content creators to diversify platforms can be a seed that Netflix uses to grow a strong UGC business. Netflix could easily be seen as a YouTube that allows for more creative expression, fielding the highest quality of user-generated content.

After all, why compete in the premium content subscription streaming space where there is a crowd of well-funded and powerful competitors (e.g. Amazon, Apple, Disney), when you can compete in a space where there is only one competitor ripe for disruption?

Lessons

Finally, to wrap this all up, let’s review some lessons we can learn from Netflix’s plight:

Moats are important. Netflix didn’t have much of a moat, yet analysts and investors heavily discounted this as a problem. As such, they also heavily discounted the impact of Netflix’s looming competition. If you read Bill Ackman’s shareholder letter on the Netflix investment, he completely ignored the competition factor.

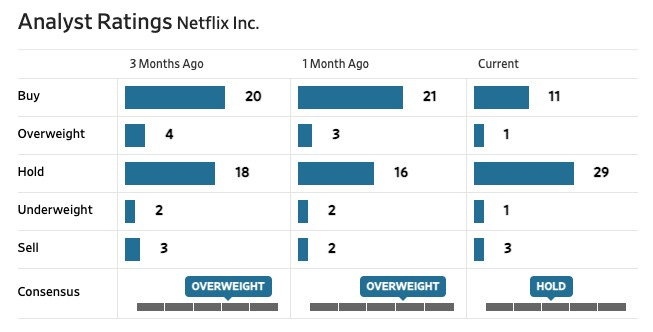

Markets can be incredibly wrong. With the fast and dramatic drawdown of Netflix’s stock price, from a peak of $700 in November of last year to about $220 today, the broad market seemed to have vastly mis-priced Netflix. In addition, prior to this drop, sell-side analysts were generally bullish for the stock, with 24 analysts having a “Buy” or “Overweight” rating, 18 with a “Hold” rating, and only 5 with a “Sell” or “Underweight” rating. As such, independent investors need to realize that market sentiment can often be highly detached from reality and can’t always be relied upon.

Beware of major investors talking up their books. Bill Ackman is a hedge fund manager overseeing a fund with almost $18.5 billion in assets under management, yet he was dead wrong with his Netflix investment. His divestment from Netflix at a massive loss shows that major investors can be wrong more often than they appear, and sometimes the loudest ones could be the wrongest ones. But, we also have to keep in mind that, as the great investor Peter Lynch said, “in this business, if you’re good, you’re right six times out of ten. You’re never going to be right nine times out of ten”. This applies to all market participants, from independent investors to major hedge fund managers.