Research - Volume Speaks Volumes

Discussing why trading volume is important and how can it be used to optimize your trading strategies.

Last year, in the midst of the meme market, a news article came out claiming that the stock of a deli shop that generated only $36,000 in sales over the past two years, with no full-time employees, was valued by the stock market at $113 million. How was this possible?

Although this valuation is technically true, it was just another mischaracterization of a situation to generate eye-catching headlines.

The deli was never worth $113 million but the reason you could technically claim this valuation is accurate is due to a tendency for people to extrapolate the worth of every single share in existence based on the recent trades of a few.

Before we dive into this, let’s quickly go over what trading volume is. Volume is simply a measure of the number of shares that were bought/sold over a given time period.

It’s a very important measure for a stock as it represents overall interest in the stock as well as its liquidity. A high volume stock is easier to trade since its high activity increases the likelihood of traders, especially those with lots of capital, to enter and exit trades at the market’s quoted price. In other words, when you want to buy or sell at the market’s quoted price, there’s usually buyer(s)/seller(s) willing to fulfill your order. In addition, because a high volume stock has so many traders and dollars involved in it, its orderbook is a lot more efficient with bid and ask prices being very close to each other at all times.

Now back to the deli. Its stock had almost no volume, yet a few of its shares managed to exchange hands for wildly high prices. A common practice to calculate a company’s market cap is to take the last traded price of a stock and multiply it by the number of shares outstanding. As such, the prices of the few shares that were traded implicitly became the price of all the other shares and a simple multiplication resulted in the $113 million valuation.

As you can see, this method of calculating market cap can be misleading, especially for low volume stocks. For example, if a little-known company with 100 million shares outstanding had one share traded at $1,000, does that mean the company is worth $100 billion? Most likely not, since no one is willing to shell out that much money for all the shares of the company.

In the deli’s case, market cap extrapolation on an extremely low volume stock enabled the proliferation of this puzzling and amusing news story of a small deli being worth an impossible $113 million.

Cash on the Side

I want to take a quick detour to discuss the concept of “cash on the side” and how a stock’s price changes based on its trading activity, which are tangentially related to volume.

A few months ago, I heard an interesting exchange on CNBC that got me thinking. It was during one of those brief market corrections in 2021 and a commentator was saying that there was a lot of cash on the side ready to buy the dip. Another commentator gave a rebuttal saying that there’s always cash on the side, since for every buyer there’s a seller that receives cash.

Without explicitly considering it, it might be easy (at least this was the case for me) to build an implicit impression that the stock market is a machine that, in aggregate, converts dollars into company shares and back. How else would statements like “Amazon is a trillion dollar company” make sense if not for one trillion dollars having been converted to Amazon stock via the stock market?

However, as we’ve discussed earlier about volume and market cap extrapolation, we know that’s not the case. Amazon is a trillion dollar company because some of its shares were recently traded at a price such that if extrapolated to all shares of the company, the company is worth a trillion dollars.

As such we reach the key question:

If there’s always cash on the side, meaning that the total cash in the stock market remains about the same in a trading day (cash just exchanges hands), how do stock prices change?

After some pondering, my understanding of this is that stock prices are indeed moved by cash, but in a subtle way. Holistically, cash works in tandem with volume and sentiment to determine a stock’s price.

How Do Stonks Go Up?

Let’s consider the case of how a stock’s price rises.

At any given point in time, a stock’s orderbook has a series of bids (i.e. a bid to buy shares) and offers (i.e. an offer to sell shares). When a trader buys shares, they will fulfill the cheapest offer on the orderbook (the top of the red column in the image above). This trade is then broadcast to the rest of the market and the stock’s price briefly updates to this trade’s price until the next trade’s price overrides this.

As such, a stock’s price can increase if a lot of cash was used to fulfill the offers in the orderbook or if the offer-side of the orderbook thins out and buyers have to fulfill more expensive offers to acquire the stock.

The orderbook is highly dynamic. If market makers notice that there is significant buying pressure, the cheapest orders will quickly be fulfilled and market makers will gradually increase the price of new offers they post. In this way, the price of the stock slowly moves up. As the rest of the market sees the price of recent trades increase, sentiment improves and more people are willing to buy the stock at this higher price.

In this way, you can see that a stock’s price can increase drastically with just a few dollars if there is low liquidity on the offer side. In other words, if few people want to sell, resulting in few offers on the orderbook, then even a small amount of cash that’s used for buying can rocket the stock’s price up to unreasonable levels by fulfilling a sparse amount of cheap offers up to super expensive offers.

This was what happened with the GME short squeeze in 2021 when the stock went from about $20 to over $300 in just a few days. There was no sell-side liquidity.

GME’s market cap increased from $1.3B to over $22B during this short squeeze but $20B didn’t just pour into the stock, the orderbook simply changed based on who wanted to buy and who wanted to sell.

How Do Stonks Go Down?

On the flipside, the same mechanisms that increase a stock’s price can decrease it. If many shares are being sold, then the orderbook will adjust and bids will gradually fall in price. If there are few interested buyers, then sellers will have to fulfill super low bids and a stock’s price can collapse quickly.

Wrapping Up

Let’s wrap up by revisiting the concept of cash on the side. Yes, there is always cash on the side since cash is simply exchanging hands for every trade and not being converted to shares or back. A stock’s price only changes based on how its orderbook adapts to imbalances in buy/sell-side volume.

Cash on the side can quickly be used to push stock prices up if it’s deployed. In other words, a trader that just sold stock can use this new cash to fulfill offers on the orderbook which will push orderbook prices up.

On the other hand, cash on the side can be hoarded and not used for buying, which will result in a drying up of buy-side liquidity and a corresponding fall in orderbook prices.

The key takeaway here is that there is always cash on the side. As far as each trade is concerned, the aggregate amount of cash in the stock market remains constant. It’s how the cash flows and how orderbooks adjust to this flow that determines stock prices.

Volume Speaks Volumes

Now that we have a better idea of how prices are set in the stock market, we can circle back to volume and specifically discuss how a stock’s historical volume can provide a wealth of information on the market’s overall sentiment of the stock and where it’s likely headed.

Interpreting Volume

At a high level, a stock’s volume at any given time can be thought of as a rough approximation of the market’s belief in the stock’s price. If the stock is trading at a certain price range and there’s high volume, this suggests that lots of traders believe this is a fair price to trade the stock at. One possible interpretation of this high volume zone is that if the stock’s price ever rises or falls from this zone, it’s likely to return to the high volume price since that’s where most people believe is a fair price.

There are other ways you can use volume to interpret price action. For example, if a stock’s price increases on relatively high volume, then that suggests that this move upwards holds weight and will continue since so many dollars (and possibly traders) are behind this move. As such, a trader could decide to buy in as well with the expectation that it’s more likely for the stock to keep going up given the high volume.

Another example is the classic consolidation phase for a stock. A consolidation phase is typically defined as a period where a stock that just experienced a significant drop in price trades at low volume in a price range for an extended period of time. This low volume suggests that the sellers have run out of steam and are met with sufficient buying volume to keep the stock’s price steady. During this time, traders start to accumulate shares until an inflection point when the consolidation phase turns into a major uptrend.

I won’t dive too much into all the different ways you can use volume to interpret price action and predict price moves. There are volumes (pun intended 😞) of material on how to use volume to trade that interested readers should definitely explore. I hope this article has whetted your appetite on the potential of incorporating volume in your trading strategies.

Volume Indicators

Before I end this article, I also want to highlight a couple useful volume indicators that can add a trove of information to your price action analyses.

A very popular volume indicator is the Volume-Weighted Average Price (VWAP). It’s basically a separate line on a stock’s price chart that represents the stock’s price weighted by volume. VWAP tends to be closer to high volume zones and further away from low volume zones and can be a better interpretation of what the market thinks is a stock’s “fair value” price at any given time. One possible way to trade using the VWAP is to go long when a stock’s price falls below VWAP and short when it goes above. This is because VWAP is where there’s more volume and thus one can argue that price will gravitate towards levels with historically higher volume.

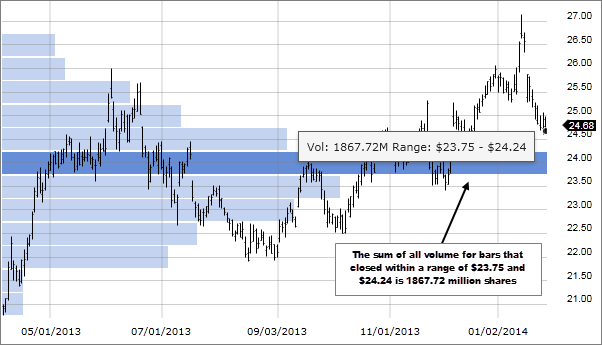

Another popular volume indicator is the Price By Volume Chart (PBV). The PBV is a horizontal histogram plotted on a stock’s price chart that shows volume traded at each price level. The more volume there is, the longer the histogram bar. The PBV is yet another view of where high and low volume zones are, and is very useful in showing traders where important price levels are.

Fin

The stock market is ultimately a measuring machine where cash is exchanged, not converted. However, traditional finance media doesn’t make this immediately clear, and many concepts are presented almost as if the stock market is actually a machine that converts cash into shares and back. Here’s a headline from CNN on May 12th: “More than $7 trillion has been wiped out from the stock market this year”. This is an eye-catching headline with a big number but we know that nothing was actually wiped out and cash just moved around, causing orderbooks to adapt. This resulted in an extrapolated market cap decrease of $7 trillion.

The bottomline is, how cash flows in the system is what actually moves the market and determines stock prices. This is why volume can be a highly valuable source of information to help traders understand the current state of the market and predict its future moves.

Here’s this week’s Market Forecast newsletter issue if you’ve missed it. I talk about the only thing that matters to the stock market. This should be an interesting and informative read.