Understand Tesla in 10 Minutes

Exploring the ins-and-outs of Tesla ($TSLA) to help you understand how the business is doing in 10 minutes.

TLDR

As of right now, Tesla is a very strong business. Revenue and net income are soaring. It has industry-leading margins. It has very little debt.

Tesla’s stock is exceptionally expensive, even after its recent massive drawdown in valuation. Its current Price to Earnings multiple is 5x larger than the second most expensive automaker, Toyota.

Tesla is not a technology or energy business, they are just distractions.

The growth story for Tesla, so far, is a company being overwhelmed with demand. This is changing fast. Growing concerns of waning demand for Tesla’s cars is placing significant pressure on its stock price.

Weak demand will devastate the stock.

As Tesla’s CEO, Musk continues to remain a wild card/surprise factor for investors shorting Tesla’s stock. Despite this, changing circumstances have emboldened an increasing number of short sellers.

Background

In 2018, a debt-ridden Tesla struck a deal with the Chinese government to build a massive factory in Shanghai. This deal came with a generous $1.4 billion loan from Chinese banks which helped Tesla stave off its domestic creditors and avoid a bankruptcy.

At the same time, the company figured out how to mass produce the Model 3.

Ever since then, the company has been growing like its strapped to a SpaceX Starship rocket, with many top level business metrics (revenue, net income, debt, margins) trending sharply in the right direction.

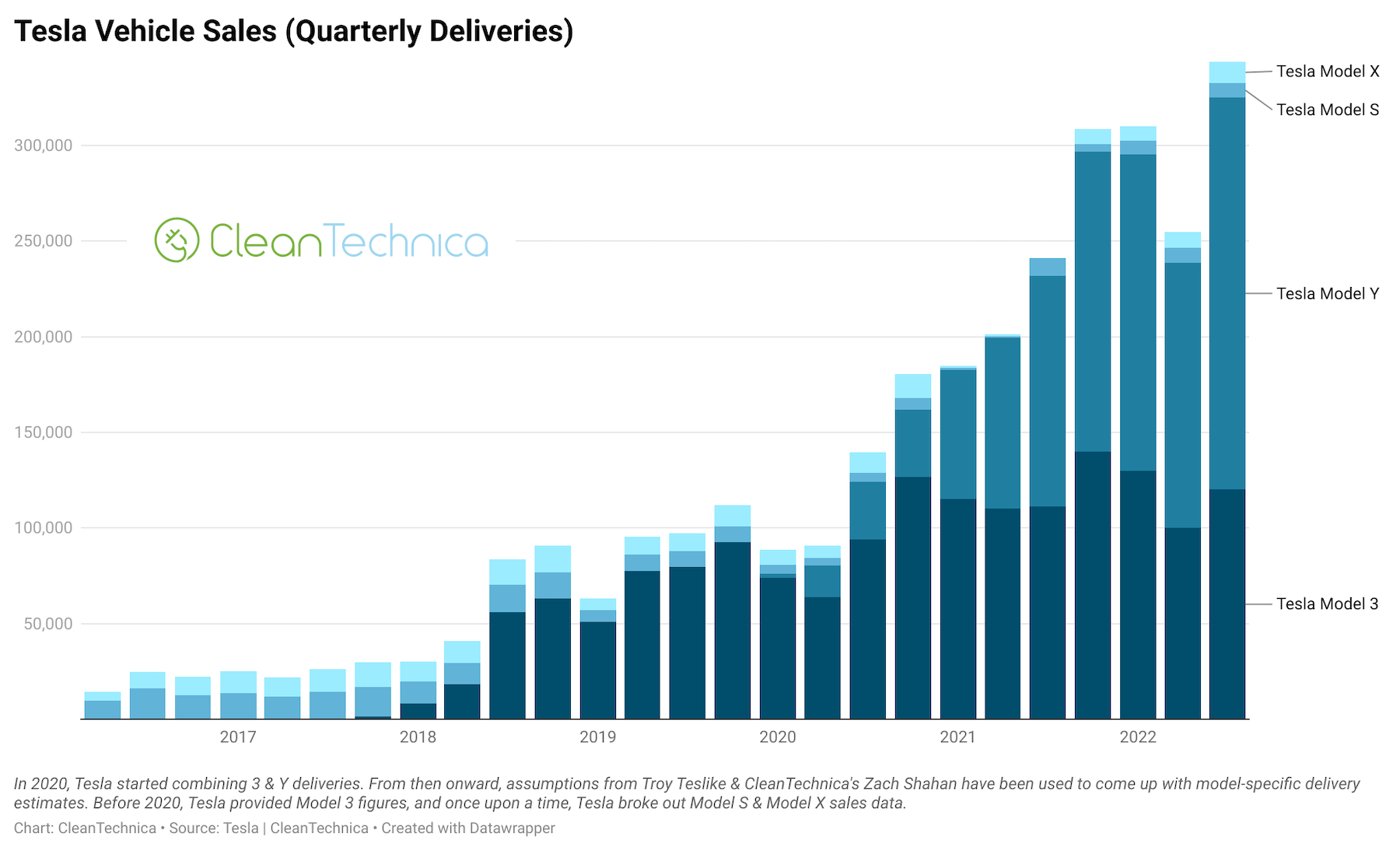

For the past couple years, the demand for Model 3s and Model Ys was huge and Tesla had one singular mission: ramp up production worldwide to meet this demand.

The company was remarkably successful in this respect and 2019 was an inflection point for the company’s valuation. Its market cap soared from around $50 billion to over $1.2 trillion at the height of the pandemic!

Strong Business, But Exceptionally Expensive

As of right now, Tesla is a very strong business. Its revenue and net income are both soaring. It has very little debt. It has industry-leading margins.

However, even with its recent massive decline in valuation ($1.2 trillion to just under $400 billion), it’s still incredibly expensive relative to its automaker peers. Its current Price to Earnings multiple is 5x larger than the second most expensive automaker, Toyota. In addition, Tesla delivers only a tiny fraction of the number of vehicles that its peers deliver.

Energy Or Technology Business?

Some claim that Tesla’s valuation is justified because it’s not just an automaker, it’s also an energy and a technology business.

We disagree.

The energy and technology business narratives are both distractions and it’s unclear when they will ever make enough of a material impact on Tesla’s top and bottom lines to justify the company’s inflated non-automaking valuation.

Not an Energy Business

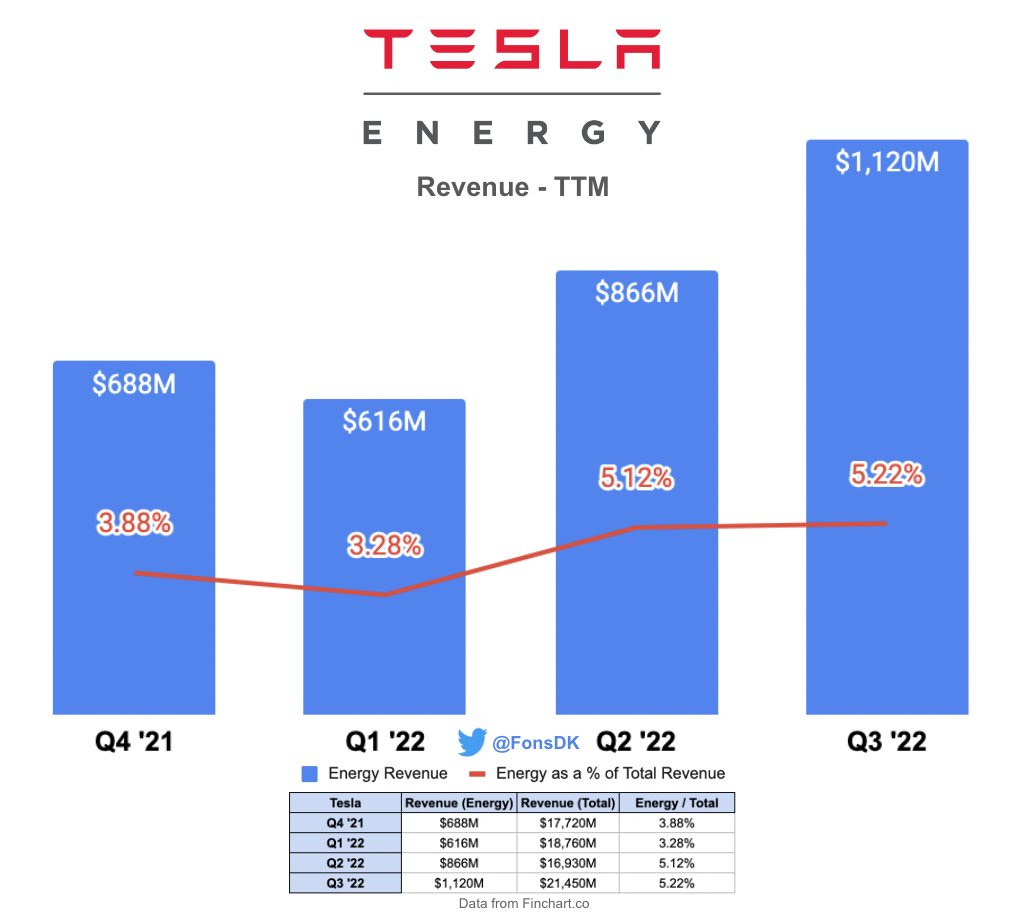

Tesla’s energy business contributes a mere 5% to its total revenue. The business is growing at around 10% year-over-year. This is far slower than expected if one were to take Elon’s grandiose claims about its eventual scale seriously.

Not a Technology Business

While GM’s Cruise is operating a paid sans-driver self-driving car service in San Francisco, Phoenix, and Austin, Tesla’s Autopilot/FSD software is under criminal investigation by the Department of Justice for the company’s dangerously inflated claims about the capability of its software. The investigation comes after a series of crashes involving Autopilot/FSD in the past year.

In Tesla’s public filings related to the criminal investigation, the company has admitted that Musk and the company had significantly exaggerated the capabilities of Autopilot/FSD.

As for the Tesla Robot, when it was announced last year, the company brought out a human dressed in a cheap black and white outfit to look like a robot and had them do silly dances. This is how far away Tesla is from a working robot, let alone one that’s AI-powered and autonomous, as touted by Musk.

So Where Are We Today?

There are two dark clouds hanging over Tesla’s stock price right now:

Weakening demand for Tesla’s cars.

Twitter: Musk being distracted with Twitter, Musk hurting his public image (and thus Tesla’s) with Twitter drama, Musk having to sell Tesla stock to support his Twitter purchase (he sold $3.5 billion last week even after saying he would stop).

The most problematic of the two concerns is weakening demand.

Tesla’s growth story has so far been about scaling up production capacity to fulfill overwhelming demand. If demand wanes, this growth story will fade and its near-term valuation will collapse.

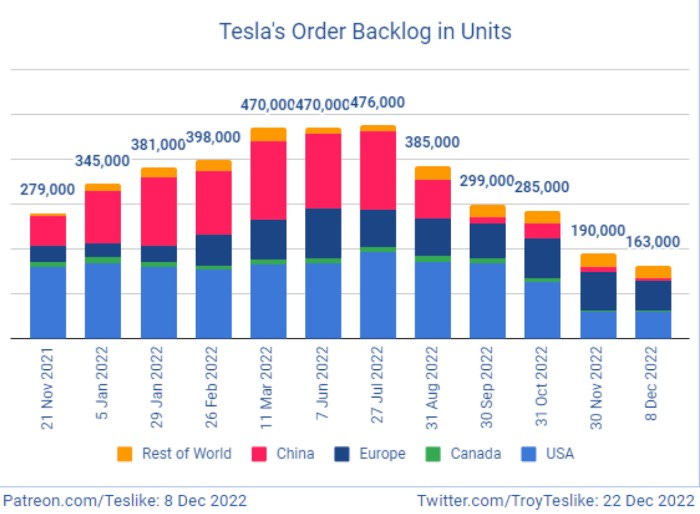

So far, signs of waning demand include a shrinking vehicle order backlog, a rumor that the Shanghai factory’s production output will be cut by 20% this month, and the sudden offering of generous discounts for its cars.

Just yesterday, Tesla’s stock fell almost 10% after news came out that the company increased their discount for Model 3 and Model Y cars from $3,000 to $7,500 while offering 10,000 miles of free supercharging. The market took this as a sign that the company is struggling with demand and is desperately trying to shore up sales by the end of the quarter.

Of all the concerns surrounding Tesla’s business today, contracting demand is the most worrisome and the most devastating. The company’s number 1 priority now should be to shore up demand. This can (possibly) be achieved by:

Fixing Tesla’s ailing public image, which has been dragged down by Musk’s Twitter escapades.

Releasing new vehicle models (e.g. Cybertruck) and redesigning existing models.

Improving overall vehicle build quality.

Expanding to new international markets, like India.

The Federal Reserve loosening financial conditions early next year. We think this is highly unlikely.

I love your reporting