The Trillion-Dollar Magic Trick

How the US Treasury found trillions of dollars of government funding that left the financial system unscathed.

Janet Yellen is Biden’s employee-of-the-year.

In a year when the US government was facing a near-record budget deficit while long-term interest rates were blowing out, Yellen devised an ingenious way to secure trillions of dollars in funding for the government without breaking the US long-term debt market.

This issue describes Yellen’s Trillion-Dollar Magic Trick.

📝 Quick note on markets today

March CPI came out today and it’s really hot.

3.5% year-over-year and 0.4% higher than February CPI, beating expectations of 0.3% higher. Core CPI painted a similar picture, 0.4% higher month-over-month and 3.8% year-over-year.

I predicted this hot CPI print in last week’s newsletter issue, Market Pulse: Between Two Giants. The SPDR Energy sector ETF rose 10% in the past month and is pushing all-time-highs. That’s gotta have an impact on inflation right?

I’m just incredibly surprised that there was so little discourse about this in financial media.

Yesterday, I put on two new trade ideas and shared them in the premium FinanceTLDR spreadsheet, short TQQQ (leveraged tech-heavy ETF) and short TLT (long-term US treasuries), because of the likelihood of a summer of high inflation. These new ideas proved prescient.

As for the existing ideas, I’m considering cutting losses on Zillow given that it’s a stock that’s highly sensitive to interest rates. Zillow is still a very good company, but the trade idea is a bit too early.

Besides a hot inflation print, Xi Jinping just met with former Taiwan President Ma Ying-jeou and said that outside interference could not stop the “family reunion”. This is in line with what was discussed in the most recent newsletter issue: China Doesn't Make Sense, Unless?

📈 Setting The Stage

Being the Treasury Secretary after a stint as a Federal Reserve Chair has its perks.

For one, it makes for a badass resume. More importantly, you have a very deep knowledge of not only how the US financial system works but also how your monetary policy counterpart, the Federal Reserve, works.

As such, it’s no surprise that amidst a serious US government budget shortfall last year that threatened to shake financial markets, Yellen deftly pulled off a sophisticated “magic trick” to secure trillions of dollars of funding for the government with minimal impact to markets.

Before we discuss how she did it, we need to set the stage to illustrate the severity of the budget crisis.

2023 came at the tail-end of a massive government spending spree to support a pandemic-ridden US economy.

Trillions of dollars were printed by the US government to back stimulus act after stimulus act. Not surprisingly, this resulted in a severe bout of inflation that forced the Fed to rapidly raise interest rates while downsizing its $9 trillion balance sheet at the same time (quantitative tightening).

🚩 The Problem

By 2023, the Fed’s monetary tightening policies were at their peak.

The Fed Funds Rate reached a high of 5.25% while $60 billion of treasuries and mortgage-backed securities were rolling off the Fed’s balance sheet each month.

At the same time, the US government’s budget was exploding as it grappled with higher interest payments from all the pandemic spending as well as soaring defense spending to support two new major proxy wars in Europe and the Middle East.

The US government faced a $1.7 trillion deficit for the year in a time when long-term interest rates were at two-decade highs.

To make matters worse, the US government’s two largest foreign sovereign treasury buyers, China and Japan, were not only cutting back on treasury purchases, but also selling treasuries (both owned about $1 trillion worth at the time).

In anticipation of this massive budget shortfall, with global US treasury demand very weak, the market sold off long-term US treasuries and both the 10-year and 30-year treasury yields rose from 3.6% in January 2023 to 5% in late October.

To put it bluntly, Yellen’s biggest problem was, how on Earth was she going to find trillions of dollars to fund the massively bloated government budget without blowing up long-term interest expenses?

Keep in mind, 5% of $1.7 trillion is $85 billion.

That’s $85 billion in extra interest payment each year for the next 10-30 years if she issued all this extra debt at the market price for long-term debt.

As we know, she somehow managed to sidestep long-term interest rates and found a trillion-dollar truckload of funding for the government with minimal impact on the long-term US debt market.

Here’s how Yellen ingeniously pulled it off.

💡 The Solution

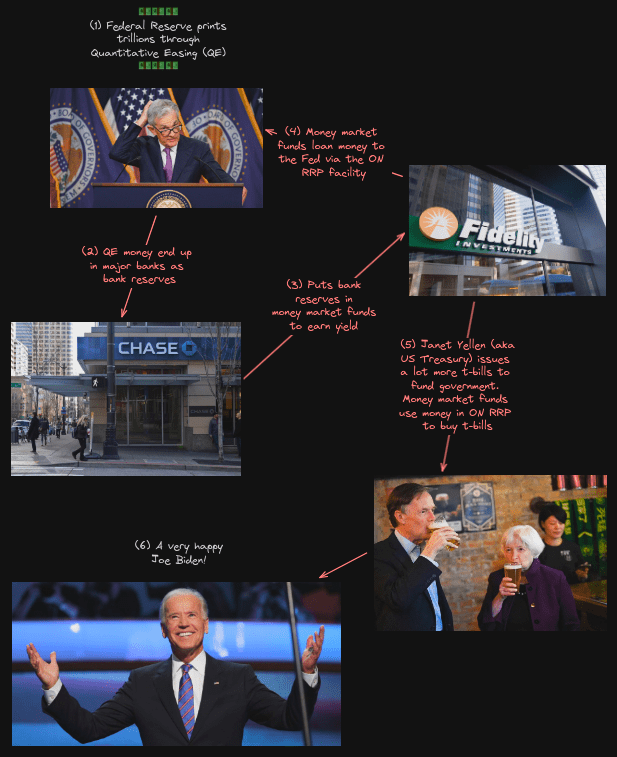

When the Federal Reserve expanded its balance sheet by $5 trillion in two years to support the pandemic economy, most of this money was introduced into the financial system as bank reserves.

The financial institutions that became flush with bank reserves directed a lot of this money to money market funds.

The money market funds, who suddenly found themselves stuffed with trillions of dollars more in assets under management, want to earn yield on this money and so loans it out to the Fed via the Fed’s Overnight Reverse Repo facility.

As such, the ON RRP’s balance rose from practically $0 at the start of 2021 to $2.5 trillion by the end of 2022.

Yellen astutely identified that this gargantuan amount of money in the ON RRP, that wasn’t there prior to the Fed’s massive expansion of its balance sheet, could be the perfect source of funding for the US government.

As such, knowing that money market funds cannot hold securities with maturities of more than 397 days, she directed the US Treasury to ramp up short-term treasury issuance (short-term treasuries are colloquially referred to as treasury bills or t-bills).

The benefits of t-bill issuance were three-fold:

For one, even though short-term interest rates were a bit higher than long-term interest rates, the government was only liable to pay the high interest on t-bills for one year.

Second, debt that’s paid for through t-bills is debt that doesn’t need to be paid for with long-term treasuries. This attenuates upwards pressure on long-term interest rates.

Finally, while international demand for long-term US treasuries has been waning, there’s a massive buyer for short-term US treasuries in the form of money market funds with $2.5 trillion of QE money parked in the Fed’s ON RRP that’s ready to buy t-bills.

As such, the US treasury got to work and began heavily increasing t-bill issuance.

The result?

A steeply-sloped gradual fall in the ON RRP balance starting mid-last-year, from just over $2 trillion to $450 million today. At the same time, long-term US treasury rates have stabilized and fallen a little bit.

So there you have it, Yellen’s masterful avoidance of the US government’s trillion-dollar budget crisis through the adept observation that the trillions of dollars in the ON RRP can be a major source of funding for the US government.

🧭 So What Now?

The money in the ON RRP may have staved off a government funding crisis for the past year but we know that it’s not a permanent solution.